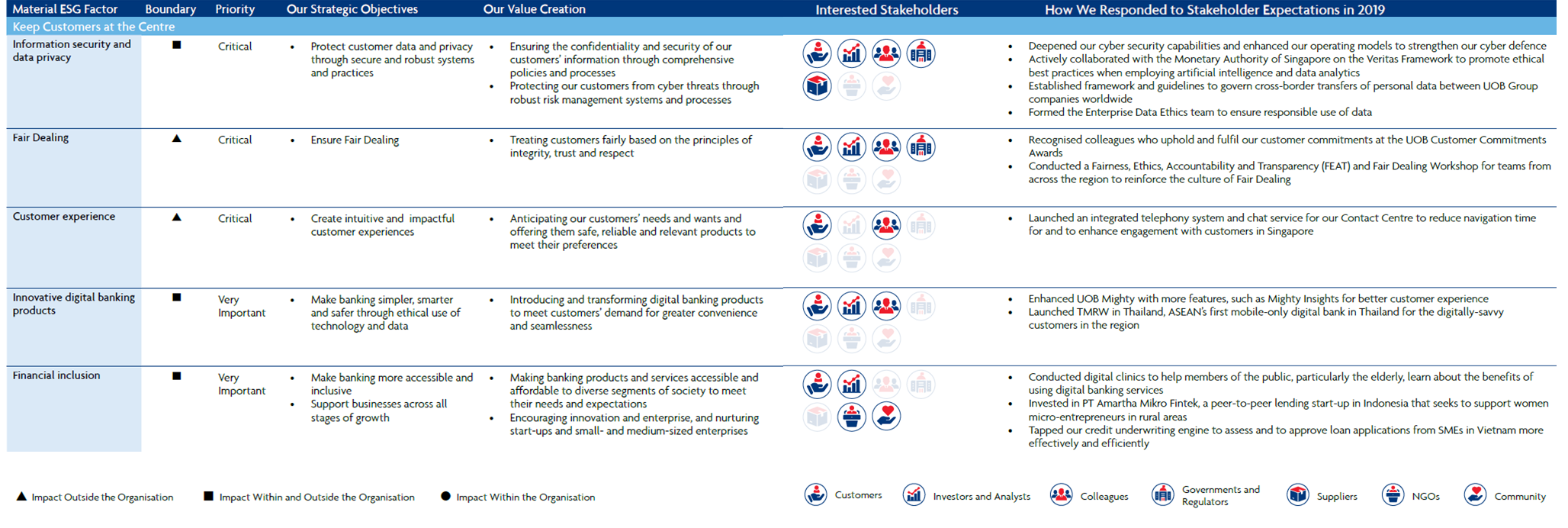

Go to pages 88-97 of our 2019 Annual Report to find out more about how we approach each of the below material ESG factors.

Click here to view the image in mobile.

you are in UOB Group![]()

Go to pages 88-97 of our 2019 Annual Report to find out more about how we approach each of the below material ESG factors.

Click here to view the image in mobile.

We use cookies to improve and customize your browsing experience. You are deemed to have consented to our cookies policy if you continue browsing our site.