UOB Group reported a 29% increase in net earnings to S$2.0 billion for the first half of 2021 (1H21) compared with a year ago, supported by its strong customer franchise and lower credit allowance as more economies reopened during the period.

Net earnings for the second quarter of 2021 (2Q21) stood at S$1.0 billion, a year-on-year jump of 43%.

Despite the uneven economic recovery across markets, UOB’s proactive and focused approach to supporting customers in their business and investment needs continued to reap positive results. Loans in 1H21 grew 6% year on year, while fee income rose 28% on the back of strong wealth management, loan-related and fund management performance.

Group Wholesale Banking’s revenue grew 5% to a record S$2.1 billion, with cross-border income up 5%. The increase was driven by the demand for financial solutions from large corporate and institutional clients, especially in Singapore, Greater China and developed markets, that are seeking cross-border trade and investment opportunities across the region. With more companies adopting sustainable business practices, their demand for sustainable financing also grew. The Group extended a total of S$13 billion in sustainable financing to its clients as at 30 June 2021.

Group Retail ’s revenue was up 1% to S$2.1 billion, despite a decline in net interest income. In 1H21, wealth management fees rose 32% and assets under management (AUM) from high affluent customers increased 7% to S$137 billion. The Group is also steering wealth to sustainable investments. As at 30 June 2021, total AUM in environmental, social and governance-focused investments was S$5.7 billion.

Overall asset quality remained resilient as the non-performing loan (NPL) ratio was stable at 1.5%. With strong pre-emptive general allowances taken previously, total credit costs normalised downwards to 24 basis points.

The Monetary Authority of Singapore lifted the dividend cap recently. Together with strong earnings and capital position, the Board declared an interim dividend of 60 cents per ordinary share. This translates to a dividend payout ratio of 50%. Post dividend, the Group’s balance sheet remains in a solid position. UOB Group will continue to see customers through to better times.

CEO Statement

Mr Wee Ee Cheong, Deputy Chairman and Chief Executive Officer, UOB, said, “Our diversified customer franchise and investment in digital capabilities have enabled us to deliver another strong set of results. We achieved a 29 per cent increase in 1H21 profit, driven by healthy contributions from our core businesses and resilient asset quality. Our performance was underpinned by our proactive and focused support for our customers in their businesses and investments.

“Our robust balance sheet and strong capital and liquidity positions also enable us to support our customers in capturing new opportunities arising from the growth momentum in Greater China and developed markets. We are accelerating our digital agenda to provide progressive solutions in anticipation of their business and personal financial needs. With countries speeding up their vaccination drive, we are optimistic that the situation will gradually pick up in Southeast Asia. In forging a sustainable future with our customers across the region, we remain committed to working with governments across the region to provide affected customers, especially small- and medium-sized enterprises, with liquidity support to see them through these tough times.”

Financial Performance

1H21 versus 1H20

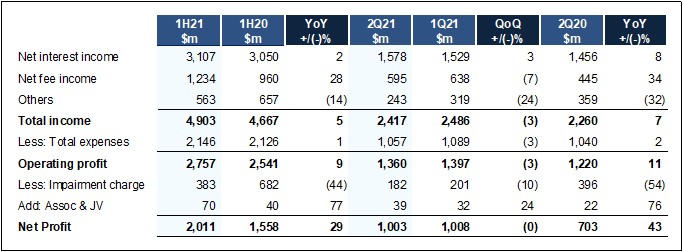

Net profit of S$2.01b in 1H21 was 29% higher from stronger business momentum and lower credit allowance. Net interest income grew 2% against last year to S$3.11 billion, led by healthy loan growth of 6% which offset the 4-basis point decline in net interest margin. Net fee and commission income rose 28% to a new high of S$1.23 billion with wealth management fees reaching record levels amid returning investor confidence on market recovery. Corporate customers were also showing confidence in the economy with increased trade and investment transactions, leading to a 33% increase in loan-related fees. Fund management and credit card fees also grew strongly on the back of the expected economic recovery and higher customer spending respectively.

Customer-related treasury income rose 9% on the back of improved business sentiment, while other noninterest income decreased 14% to S$563 million due to lower non-customer trading income.

While total income grew 5% year on year, total expenses was stable at S$2.15 billion as the Group continued to maintain cost discipline. The cost-to-income ratio for the year improved from 45.6% to 43.8%.

Total allowance fell to S$383 million from S$682 million a year ago, as asset quality remained within expectations with strong reserve coverage from the proactive general allowance taken in last year. Total credit costs on loans decreased from 52 basis points to 24 basis points.

2Q21 versus 1Q21

Net interest income increased 3% to S$1.58 billion alongside loan growth. Net fee and commission income decreased 7% to S$595 million, largely due to lower wealth management and fund management after an exceptional 1Q21. Trading and investment income declined 26% to S$182 million as the last quarter benefitted from higher gains on investments.

Total operating expenses decreased 3% to S$1.06 billion. Total allowance fell 10% to S$182 million from lower general allowance, while specific allowance was higher from a few corporate accounts.

2Q21 versus 2Q20

Net interest income increased 8% led by robust loan growth of 6% and an 8-basis point increase in net interest margin to 1.56%. Net fee and commission income grew 34%, driven by strong growth in wealth management, loan-related and fund management fees. Other non-interest income declined 32% to S$243 million, mainly from a drop in non-customer-related gains.

In tandem with strong income growth and disciplined cost management, the cost-to-income ratio improved from 46.0% to 43.7%. Total allowance more than halved to S$182 million as much of the pre-emptive general allowance was taken last year.

Asset Quality

Asset quality remained resilient with NPL ratio at 1.5% for 2Q21, unchanged from the previous quarter. The non-performing assets coverage remained strong at 110% or 265% after taking collateral into account. Total general allowance for loans including regulatory loss allowance reserves (RLAR) was prudently maintained at 1% of performing loans.

Macroeconomic conditions were more positive this year, with optimism over the region’s path to recovery albeit an uneven one. Nonetheless, as new NPLs remained low, the Group will maintain strong general allowance in anticipation of a range of possible macroeconomic outcomes.

Capital, Funding and Liquidity Positions

The Group’s liquidity and funding positions remained robust with 2Q21’s average all-currency liquidity coverage ratio at 131% and net stable funding ratio at 123%, well above the minimum regulatory requirements. The loan-to-deposit ratio was stable at 86.9%.

As at 30 June 2021, the Group's Common Equity Tier 1 Capital Adequacy Ratio remained strong at 14.2%. Leverage ratio of 7.4% was more than two times above the regulatory requirement.