You are now reading:

UOB Business Outlook Study 2026 (Hong Kong) H1: Businesses are doubling down to improve resilience for an uncertain future

Find out how we can help you fast-track your investments in the JS-SEZ.

Learn moreyou are in UOB ASEAN Insights![]()

You are now reading:

UOB Business Outlook Study 2026 (Hong Kong) H1: Businesses are doubling down to improve resilience for an uncertain future

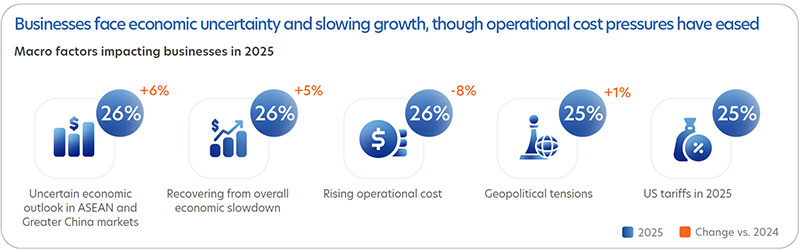

Hong Kong businesses continue to operate in a challenging environment. While concerns about rising operating costs have eased somewhat compared with previous years, economic uncertainty, a slower-than-expected recovery, and ongoing geopolitical pressures remain significant obstacles to growth.

The impact of these challenges is not felt equally across the economy. Businesses in Consumer Goods & Wholesale Trade (37 per cent) and Tech, Media & Telecom (32 per cent) are among the most affected by economic uncertainty. Meanwhile, Medium Enterprises are significantly more impacted by these challenges given their smaller capacity to absorb shocks. Half of Medium Enterprises say they are extremely affected by the geopolitical impact on supply chains.

Yet, business sentiment among Medium and Large Enterprises has rebounded following the easing of US tariff pressures, though it remains about 10 percentage points weaker than 2024 levels. Businesses in the Health, Community & Personal Services sector are leading the rebound, demonstrating resilience despite supply chain and geopolitical shocks. Meanwhile, businesses in the Tech, Media & Telecom sector are showing significantly weaker business sentiment as they struggle with rising operating costs.

Amid ongoing macroeconomic uncertainty, the UOB Business Outlook Study 2026 reveals that:

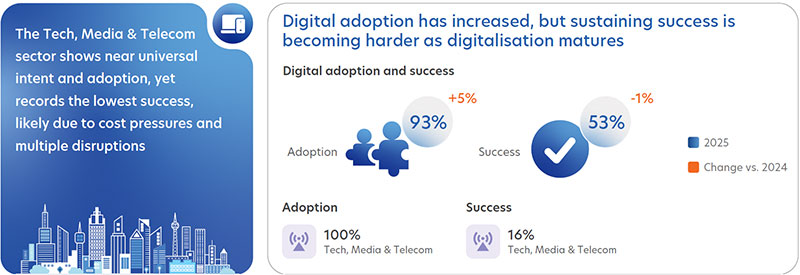

Digitalisation is now firmly embedded within Hong Kong's business landscape. Nine in ten businesses have adopted digital technologies in at least one business function, making digitalisation a baseline capability across industries. Businesses clearly recognise the value digitalisation can deliver. The most commonly cited benefits include improved productivity (36 per cent), enhanced customer experiences (33 per cent), and stronger data-driven decision-making capabilities (30 per cent).

However, not all businesses are seeing the fruits of their digitalisation efforts. Construction & Real Estate and Large Enterprises see considerable success with their digitalisation efforts. Tech, Media & Telecom, despite leading in terms of digital maturity, witnessed the least success with their digitalisation efforts due to the impact of cost pressures and multiple disruptions. Meanwhile, Medium Enterprises lag in realising successful outcomes, citing issues around costs, cybersecurity, and system capability.

Nevertheless, confidence in digitalisation remains high. Eight in ten businesses plan to increase digital investments in 2026, with many expecting spending on digital solutions to rise by 10 and 50 per cent compared to 2025, signaling continued spend momentum despite uneven success.

The rapid rise of artificial intelligence is the next phase of digital transformation across Hong Kong.

Around one in two businesses are in early or advanced stages of AI adoption, with Tech, Media & Telecom and Medium Enterprises ahead of the curve and Consumer Goods and Wholesale Trading trailing behind, in line with their digitalisation efforts. This suggests that digital maturity is linked to the pace of AI adoption.

AI adoption in the Tech, Media & Telecom sector is likely driven by a combination of available funding and access to skilled talent capable of implementing and managing AI initiatives. Strong involvement from senior leadership also appears to be a key factor in successful adoption. Businesses that have progressed to more advanced stages of AI implementation are more likely to have top management directly involved in deployment efforts.

Current AI applications are concentrated in areas that deliver immediate efficiency and productivity gains. The most common use cases include customer support (39 per cent), Generative AI applications (35 per cent), documentation processes (31 per cent), and recruitment (31 per cent).

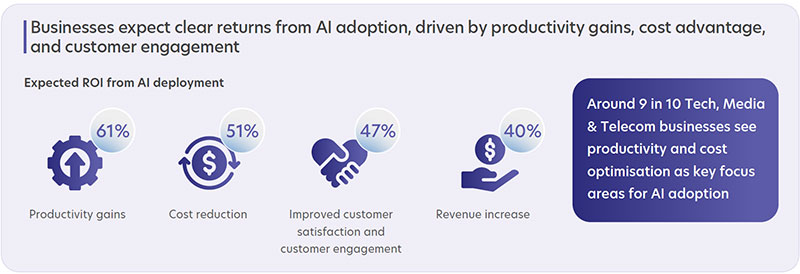

Importantly, businesses are beginning to see measurable returns from these investments. Productivity improvements, cost reductions, and enhanced customer engagement are emerging as clear outcomes, strengthening confidence in scaling AI investments. As a result, nine in ten businesses plan to increase their AI budgets in 2026, with the strongest investment intentions coming from Tech, Media & Telecom companies and Large Enterprises.

However, challenges remain. Data readiness, system compatibility, and financial constraints continue to be the primary barriers to broader AI adoption, particularly among organisations with less mature digital foundations.

Sustainability has become a strategic priority for businesses across Hong Kong. In 2025, close to nine in ten businesses identified sustainability as important to their organisation – about five percentage points higher overall compared to 2023. One in two businesses have implemented sustainability initiatives, with Tech, Media & Telecom leading adoption rates.

There is a notable shift in how businesses view sustainability: adopting it is now less about optics and more about achieving tangible benefits, such as gaining a competitive advantage (38 per cent), building a more sustainable future (35 per cent), and attracting investment opportunities (35 per cent). The importance of sustainability for attracting investments has increased significantly since 2023, reflecting growing investor expectations around environmental performance.

Operational efficiency is also emerging as a major driver. Many businesses recognise that sustainability initiatives can support cost optimisation while improving access to green financing and sustainability-linked funding opportunities.

Despite this progress, adoption barriers remain. Upfront costs, implementation complexity, and uncertainty around execution continue to slow sustainability efforts for some organisations.

Within the broader sustainability agenda, energy efficiency has become a major area of focus, driven by the overall sustainability agenda of the government. This includes its advance towards its long-term carbon neutrality ambitions through the Climate Action Plan 2050, alongside new regulations, energy-efficiency initiatives, retro-commissioning programmes, and stricter appliance energy-labelling requirements.

As such, nine in 10 businesses across sectors and irrespective of business size acknowledge energy management as important, driven by its cost savings and regulatory focus on Environmental, social, and governance (ESG). Businesses are particularly interested in reducing energy consumption (46 per cent), optimising energy usage through digital tools (43 per cent), and lowering energy costs (40 per cent).

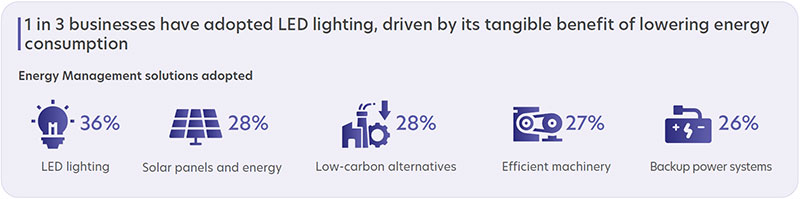

LED lighting remains the most widely adopted solution, with one in three businesses implementing it due to its immediate and measurable impact on energy consumption. Other solutions, such as solar energy systems and smart energy management tools, tend to be more sector-specific, with stronger adoption among Tech, Media & Telecom businesses and Construction & Real Estate companies.

While interest is growing, high upfront investment costs and uncertainty regarding return on investment continue to present adoption challenges.

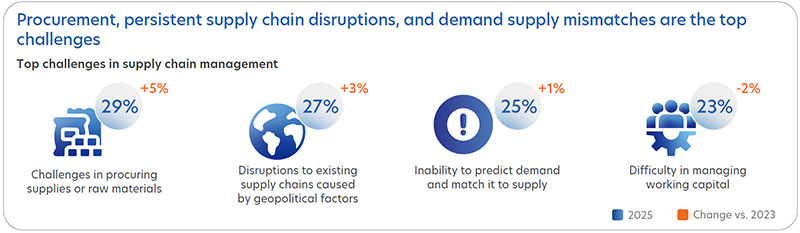

Supply chain management remains a critical concern for businesses across all sizes in Hong Kong, particularly for organisations that rely heavily on imported materials, specialised expertise, or international suppliers.

Years of disruptions have reinforced the importance of supply chain resilience. Procurement challenges, ongoing disruptions, and unpredictable demand patterns continue to rank among the top supply chain concerns since 2024.

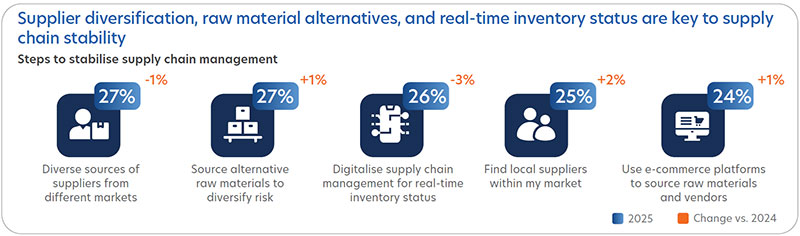

To strengthen resilience, businesses are focusing on three key strategies: supplier diversification, identifying alternative raw material sources, and increasing digitalisation to improve visibility and access to real-time information.

Supplier diversification is emerging as the most widely adopted approach. Nearly seven in ten businesses plan to expand their supplier base in 2026, with a strong focus on ASEAN markets. While only one in three businesses plans to establish new manufacturing facilities, ASEAN remains the preferred destination among those pursuing expansion. Businesses are primarily motivated by access to new markets and opportunities for cost optimisation.

The growing attractiveness of ASEAN is also supported by expanding intra-ASEAN trade, continued policy liberalisation, and strengthening economic ties between China and ASEAN markets, creating new opportunities for regional supply chain strategies.

Despite ongoing uncertainty, business expansion plans remain robust. One in two businesses expanded internationally in 2025, with Mainland China, Taiwan, and ASEAN markets serving as the primary destinations.

Eight in ten businesses remain interested in overseas expansion over the next three years, led by Tech, Media & Telecom and Large Enterprises. Within ASEAN, Singapore emerges as a top choice for future expansions, especially among Large Enterprises.

Expansion is no longer driven solely by profitability considerations. Businesses increasingly view international expansion as a strategy for revenue growth and risk diversification, particularly among Medium Enterprises seeking to reduce exposure to local market uncertainties.

However, businesses continue to face several obstacles. Finding trustworthy partners remains a major challenge, alongside securing sufficient financing and accessing the knowledge needed to successfully enter new markets.

Partner selection is becoming particularly important amid rising concerns about scams, operational risks, and uncertainty. These concerns are especially pronounced among businesses in Professional & Business Services (44 per cent) and Consumer Goods & Wholesale Trade (42 per cent).

Foreign direct investment (FDI) activity also remains strong. Two in three businesses plan to undertake FDI within the next 12 to 24 months, with ASEAN and Mainland China emerging as the most attractive destinations. Average planned investments are approximately US$14 million.

Businesses are primarily motivated by supply chain de-risking (55 per cent), lower operating costs (40 per cent), and access to talent ecosystems (38 per cent), highlighting the increasingly strategic role that international expansion plays in long-term business planning.

Businesses in Hong Kong must navigate multiple pressures at once. Instead of pulling back, they are doubling down on strategies that can improve business resilience for an uncertain future.

"In a measured business environment, Hong Kong companies are placing greater emphasis on resilience, while continuing to pursue selective growth through diversification, digitalisation, and sustainability. As they look to opportunities in Mainland China and ASEAN, Hong Kong’s role as a strategic gateway connecting these markets remains critical. Leveraging our strong regional network and deep market expertise, we are well placed to support customers in navigating uncertainties and capturing cross-border opportunities with confidence."

George Tung, CEO of UOB Hong Kong.

With UOB’s regional expertise – covering tailored financial solutions, sustainable financing, and cross-border trade support – we can help Indonesian businesses navigate an increasingly complicated environment, while opening doors to further growth and success. Contact us to find out more.

The UOB Business Outlook Study 2026 (Hong Kong) H1 surveyed 255 business owners and senior executives from Medium and Large Enterprises in Hong Kong. Conducted online in January 2026 the study offers insights into:

The H1 2026 edition also introduces three new Pulse Topics, offering deeper insights into emerging business priorities:

This article shall not be copied or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

Get the UOB Business Outlook Study 2026 (Hong Kong) H1.Download now