With the uneven flattening of COVID-19 curves across Asia and globally, it remains to be seen if there is enough momentum for a rebound to be sustained.

Asia will see a dismal year of shrinking output in 2020 under the weight of COVID-19 pandemic. As lockdown restrictions are eased and life gradually moves towards normal, real GDP growth is expected to return to positive across the world.

Based on current conditions, it would be at least 2022 at the earliest for regional economic activities to recover sufficiently and return to the pre-pandemic levels.

Asian economies have generally moved past the worst of the slump in economic activities seen in 1H20, as many governments are loosening gradually and cautiously the stringent COVID-19 lockdown measures. Assuming this tentative recovery is able to hold and not be disrupted by another wave of COVID-19 infections, we expect overall economic growth in Asia to return to positive in 2021. This report explores the impact of COVID-19 in ASEAN through various lenses such as GDP, imports and exports, foreign direct investments and tourism.

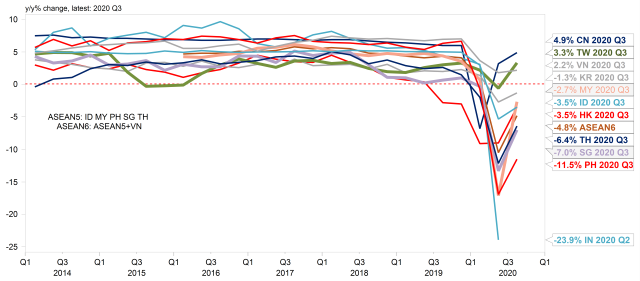

Chart 1: Impact of COVID-19 on ASEAN's economy

ASEAN's real GDP growth rates (quarterly). Source: Macrobond, UOB Global Economics & Markets Research

In general, the quicker a government could get COVID-19 under control, the faster "normal" activities could resume. Those economies which could contain COVID-19, in general, stand a much better chance to return to normal earlier. China is the prime example of this, which began restarting in 2Q20 and saw its economic growth returning to positive in that quarter, while the rest of the world was still struggling under the weight of COVID-19 lockdown measures.

The other example is Vietnam which was able to get a grip of the disease at a very early stage, although that effort was thwarted when a streak of new local infections emerged in the central city of Danang in early August.

Based on high frequency data, there are signs of a tentative recovery in Asia starting from 3Q20. China, Taiwan and Vietnam reported positive GDP growth while the other ASEAN countries reported a stronger rebound compared to 2Q20. Overall, ASEAN-6 is seeing a 4.8 per cent year-on-year decline in 3Q20.

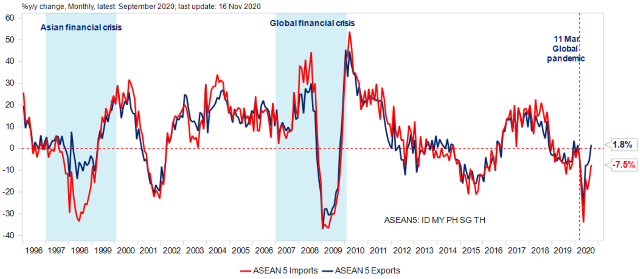

Chart 2: Exports rebound while imports remain weak

ASEAN's trade performance. Source: Macrobond, UOB Global Economics & Markets Research

Unlike the long-drawn trade slumps in previous crises, a rapid rebound in exports from the deep declines in April was seen across most markets. However, the weakness in imports suggests poor domestic demand given the uncertainty in income and employment.

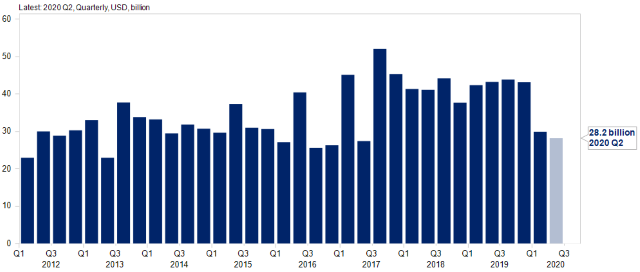

Chart 3: Foreign direct investment (FDI) inflows lower but stabilising

ASEAN: Foreign Direct Investment (FDI) inflows slowed to weakest in five years, as COVID-19 pandemic hit in 1Q20. Source: Macrobond, UOB Global Economics & Markets Research

While foreign direct investment (FDI) inflows to ASEAN have slowed in response to the global pandemic, it has stabilised at 29 per cent of the average inflows in 2019.

The drop in FDI inflows to ASEAN is largely due to sharply lower flows to Singapore, which fell 30 per cent from 2019's average, as well as Malaysia (-73 per cent), although Vietnam and Cambodia fared relatively well in 1H20.

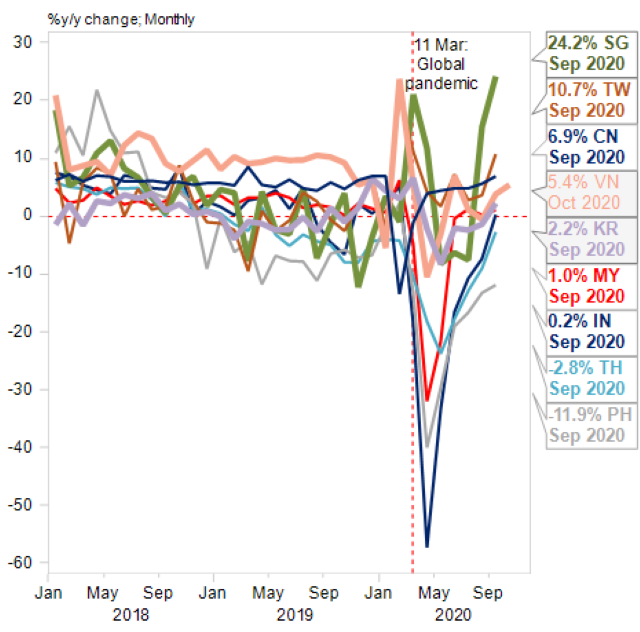

Chart 4: V-shaped rebound in industrial production output

Asia's Industrial Production Index (monthly). Source: Macrobond, UOB Global Economics & Markets Research.

Production activities, in general, have rebounded off the slump earlier this year and some have already turned positive, led by Singapore, Taiwan and China. However, with the uneven flattening of COVID-19 curves across Asia and globally, it remains to be seen if there is enough momentum for the rebound to be sustained.

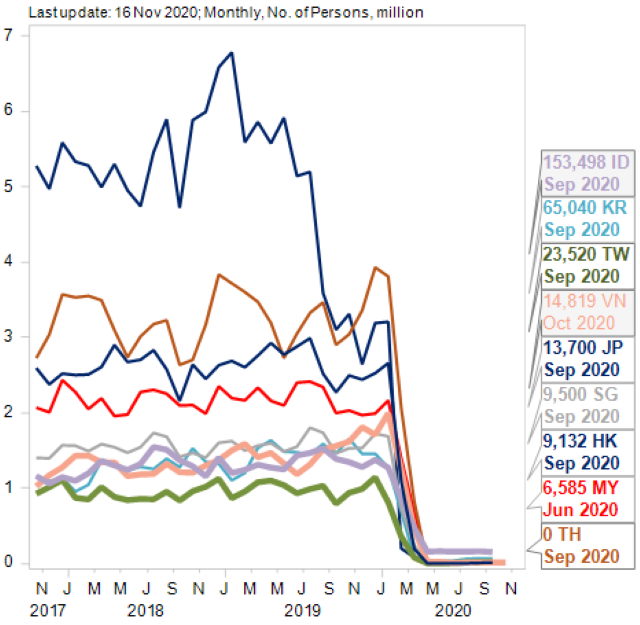

Chart 5: Where are the tourists?

Asia: Inbound tourist arrivals. Source: Macrobond, UOB Global Economics & Markets Research

Cross-border travel and tourism activities have essentially ground to a halt for most parts of 2020 due to lockdown measures to contain the spread of the COVID-19 pandemic. These activities are unlikely to resume anytime soon, or at least not before a safe and effective vaccine can be made available. This is especially difficult for those with large exposures to the travel-related businesses, including Thailand and Hong Kong.

The collapse in the tourism business is most evident in Thailand, which reported the fourth executive month (including July) of zero inbound tourists. Other popular Asian destinations reported sharply lower YTD inbound visitor figures compared to last year, with no signs of turning around anytime soon.

Thailand is most dependent on inbound visitors among the Asian economies, with tourism revenue of US$62 billion in 2019, or nearly 12 per cent of Thailand's GDP, thus underscoring the severe impact of COVID-19 on Thailand.

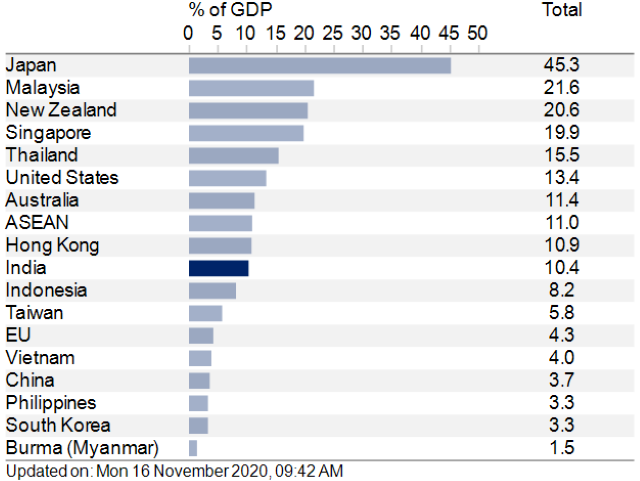

Chart 6: Swift fiscal and monetary policy responses offset some losses

Fiscal response to COVID-19 (% of GDP). Source: Macrobond, UOB Global Economics & Markets Research

Governments and central banks have reacted swiftly to cushion the fallout from the sudden shocks to their respective economies, especially during the most severe phase in 2Q20. Broadly, fiscal policy measures generally take the forms of direct cash handouts, support to workers' wages, costs reductions for businesses, and low-cost financing/loan payment moratoriums of consumers and businesses' loans.

Those governments that are able to afford, take the most aggressive approach, ranging from a low of one per cent of GDP to Japan's 45 per cent of GDP. Most other governments' support packages came in around 10 to 20 per cent of GDP, balancing the need to ensure social stability and fiscal constraints. Collectively, ASEAN member states have pumped in more than US$300 billion of fiscal support or 11 per cent of ASEAN's GDP.

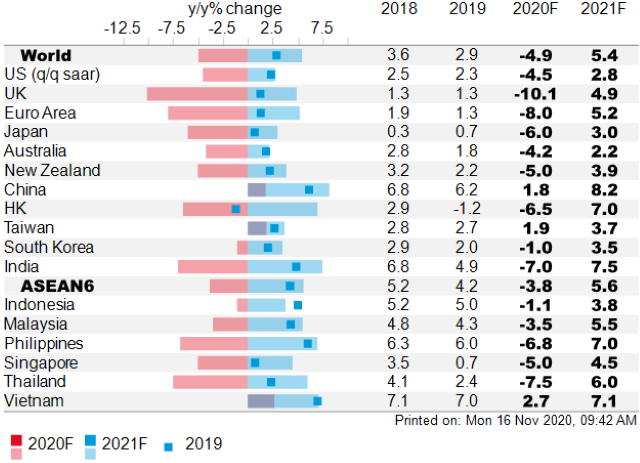

Chart 7: ASEAN's current GDP and 2021 projection

Real GDP growth rates (annual). Source: Macrobond, UOB Global Economics & Markets Research

With the exception of China, Vietnam, and Taiwan, Asia will see a dismal year of shrinking output in 2020 under the weight of COVID-19 pandemic. As lockdown restrictions are eased and life gradually moving towards normal, real GDP growth is expected to return to positive across the world. Note that, the average growth rate of 2020 and 2021 will still be far below trend for most economies.

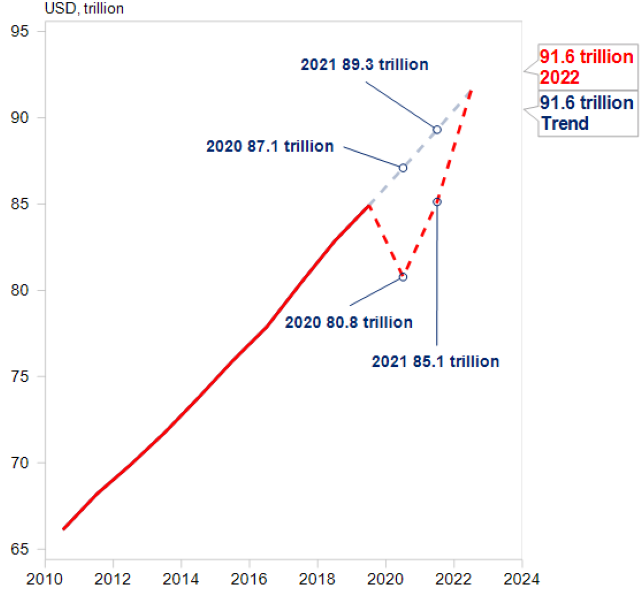

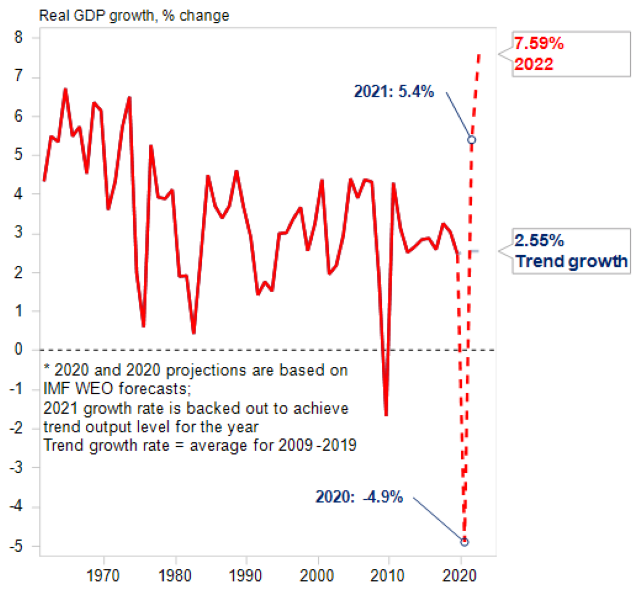

Charts 8 and 9: When can we get back to pre-pandemic output levels?

Global economy: Knocked off track by COVID-19. What does it take to get back to "normal" in 2022? Source: Macrobond, UOB Global Economics & Markets Research

Based on IMF's projections for 2020/2021, real output losses (i.e. deviation from trend output) globally could cost at least US$10 trillion in these two years. This is equivalent to output destruction in excess of US$400 billion a month, or the loss of the entire Norway's GDP every month in 2020 and 2021.

Global economy: IMF forecasts for real GDP growth* Source: Macrobond, UOB Global Economics & Markets Research

In order for global output to return to trend levels in 2022, global real growth rate would have to reach 7.6 per cent in that year. While this is possible, the chances are quite slim as such strong growth pace has not been seen before in the past five decades for the global economy. In addition, governments, businesses and consumers would be deeper in debt as they emerge from the pandemic to be able to spark off another growth spurt. As such, it would be at least 2022 at the earliest for economic activities to recover sufficiently and return to the pre-pandemic levels.

This article shall not be copied, or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

Find out how we can help your business expand across ASEAN Get in touch