Singapore 2023 Budget: Developing local enterprises, upskilling workers

Economic Outlook

15 Feb 2023

8 mins read

You are now reading:

Singapore 2023 Budget: Developing local enterprises, upskilling workers

Key takeaways

Singapore’s Budget FY2023 was tabled in an environment of sustained higher inflation, rising business costs and higher economic uncertainty and volatility. Themed Moving Forward in a New Era, this is the first post-pandemic budget as Singapore lifted its remaining COVID-19 measures on 13 Feb.

Comprehensive measures were announced to help cushion the impact of higher inflation and build capabilities in local enterprises. Notably absent, however, were further measures to advance Singapore’s green transition ahead of the increase in Singapore’s carbon tax from 2024. Another one was the lack of measures to address the ongoing manpower issues.

With Singapore moving into COVID-19 endemicity, the long-term solution for businesses will continue to be in the areas of improving their productivity through upskilling/reskilling of workers, technology and digitalisation.

Comprehensive measures to support companies and build capabilities

Singapore’s economy has continued to recover from the COVID-19 pandemic over the last two years, with the real GDP rebounding by 3.6 per cent in 2022 and 8.9 per cent in 2021 from -3.9 per cent in 2020. The labour market is now tighter than pre-pandemic as the overall and resident unemployment rates (seasonally adjusted) fell to 2 per cent and 2.8 per cent respectively in December while employment gains over the past two years (+273,100) more than offset job losses in 2020 (-166,600).

In 2023, the Ministry of Trade and Industry (MTI) is expecting GDP growth to slow to the range of “0.5-2.5 per cent” while we forecast a modest rise of 0.7 per cent (closer to the lower end of the official forecast). Meanwhile, the official forecast for core inflation is at 3.5–4.5 per cent and CPI-All Items inflation at 5.5–6.5 per cent for 2023 after factoring in the 1 percentage point increase in the Goods & Services Tax (GST) that came into effect on 1 January 2023.

Singapore’s Budget FY2023 was tabled in an environment of sustained higher inflation, rising business costs and higher economic uncertainty and volatility. It is also the first post-pandemic budget as Singapore lowered its Dorscon level from yellow to green with the remaining of its COVID-19 measures lifted on 13 February 2023.

Deputy Prime Minister and Finance Minister, Mr Lawrence Wong, announced a suite of strong and comprehensive measures to not only help cushion the impact of GST and address demographic challenges, but to also support and build capabilities in local enterprises, help them expand globally as well as fuel innovation activities.

Notably absent were further measures to advance Singapore’s green transition including more support to local companies ahead of the sharp increase in Singapore’s carbon tax from 2024. Another one was the lack of measures to address the ongoing manpower issues (including labour shortages and rising labour costs) impacting many businesses, including the in-person services sectors, although we do note that the dependency ratio ceiling (DRC) was not mentioned in the Budget, implying that there would at least be no further tightening for any sector this time round.

All in all, the measures were comprehensive and broadly addressed the most pertinent concerns of both individuals and businesses. The three key thrusts in Budget FY2023 are 1) Support measures for Singaporeans, 2) Growing our economy and equipping our workers, and 3) Strengthening our social compact. This article will focus on the second thrust and highlight key business insights from the Budget report.

Growing the economy and equipping workers

With Singapore moving into COVID-19 endemicity and further recovery expected in the pandemic-hit sectors including F&B, retail, travel, and construction this year, there are other more pressing issues such as manpower shortages and rising costs. The long-term solution for businesses, especially in labour-intensive industries, will continue to be in the areas of improving their productivity through upskilling/reskilling of workers, technology, and digitalisation.

Supporting businesses: To further sharpen the competitiveness of local businesses and nurture innovation, the Government has announced further support under the Singapore Global Enterprises initiative (S$1 billion injection), the SME Co-Investment Fund (S$150 million injection), and the National Productivity Fund to develop local companies and help companies expand globally. A new Enterprise Innovation Scheme was also announced to support businesses' innovation activities via enhanced tax deductions/allowances, with a cash conversion option. This reflects the Government’s continued commitment to encourage R&D and innovation.

Supporting workers: There are also a number of measures targeted at upskilling, reskilling as well as uplifting the lower-income group. Notably the Government announced a top-up of S$2.4 billion to the Progressive Wage Credit Scheme (PWCS) fund introduced in Budget FY2022 to co-fund eligible wage increases in 2023.

Measures such as the extension of Senior Employment Credit and Part-time Reemployment Grant for senior workers till 2025 will help to address concerns over Singapore’s ageing workforce. The Government will also provide incentives for the employment of persons with disabilities and ex-offenders as it moves towards a more inclusive society.

Easing cost pressures: To help businesses deal with the cost pressures, the Government has announced an extension of the Enterprise Financing Scheme enhancements till 31 March 2024 to facilitate firms’ access to credit. Similarly, the Energy Efficiency Grant will also be extended till 31 March 2024 for SMEs in food services, food manufacturing, and retail sectors to adopt energy-efficient equipment, given higher electricity prices.

Base erosion and Profit Shifting Initiative (BEPS 2.0)

Changes to the corporate tax system will have far-reaching consequences for Singapore’s biggest tax revenue component. DPM Wong said that the Government intends to implement Pillar 2 from 2025, as part of the broader international move to align minimum global corporate tax rates for large multinational enterprises (MNEs). Concurrently, a Domestic Top-up Tax (DTT), which will top up the MNE groups’ effective tax rate in Singapore to 15 per cent will be implemented. These will continue to be reviewed and updated to ensure Singapore remains competitive in attracting and retaining investments.

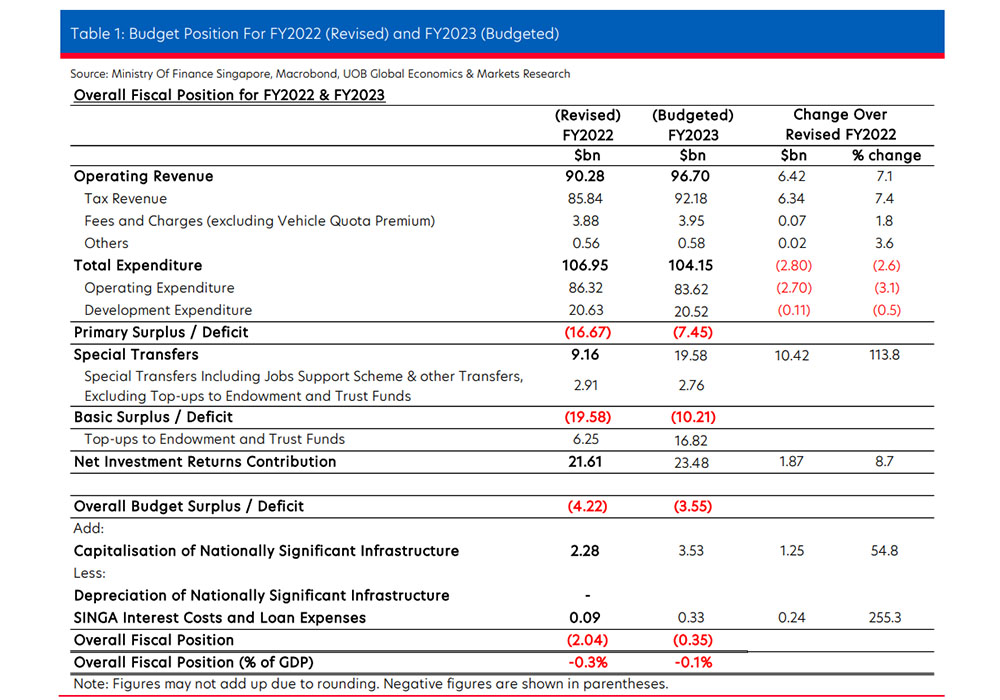

FY2022 and FY2023 fiscal position

The Government reported an overall deficit in its fiscal position for FY2022 of S$2 billion (-0.3 per cent of GDP) which is marginally smaller than its initial budgeted deficit of S$3 billion (-0.5 per cent of GDP). In comparison, we were anticipating a balanced position due to the stronger economic recovery and the stronger revenue especially from corporate and personal income tax.

For FY2023, Singapore is projected to continue to register a small fiscal deficit of S$0.4 billion (-0.1 per cent of GDP). This slightly expansionary stance budgeted for 2023 is in line with an uncertain global environment amid still elevated inflation. Having said that, should the economy turn out to be stronger than expected, a more favourable revenue collection could turn the FY2023 fiscal position to a small positive. With FY2023 being the third year of the current five-year term and deficits reported in the past two years, there will be pressure for the Government to return to a fiscal surplus position by 2024.

Fiscal sustainability is one of the top priority areas as Singapore emerges from the COVID-19 pandemic. Singapore had drawn on past reserves from FY2020 to FY2022 of an estimated S$40 billion to fight the pandemic, smaller than the initial planned withdrawal of S$52 billion. Further indicating fiscal discipline, the Government will be reducing the balance of the Contingencies Funds from S$16 billion to S$6 billion as the economy returns to normalcy, although this is still above S$3 billion prior to the COVID-19 pandemic.

However, DPM Wong said that unlike during the Global Financial Crisis when Singapore similarly drew on past reserves (S$4 billion then), the Government is unlikely able to replenish the withdrawal this time round due to its tight fiscal position. Notably, past reserves contribute significantly to the Net Investment Returns Contribution (NIRC) which at 3.5 per cent of GDP per annum over the last five years, will support about one-fifth of government spending. Faced with rising spending needs (see ), which is forecast to increase to around 19-20 per cent of GDP in the FY2026-30 period (currently around 18 per cent of GDP), and possibly exceed 20 per cent of GDP by FY2030, we expect the Government to continue to maintain its prudent fiscal approach ahead.

Budget position for FY2022 (revised) and FY2023 (budgeted). Source: Ministry of Finance Singapore, Macrobond, UOB Global Economics & Markets Research

Summary of key fiscal measures

For Businesses

For Workers

Developing local enterprises

S$1 billion of customised support for promising local companies under Singapore Global Enterprises initiative

Additional S$150 million via SME Co-Investment Fund to invest in promising SMEs

Building capabilities and anchoring quality investments

Top up S$4 billion to National Productivity Fund

Nurturing and sustaining innovation

Introduce Enterprise Innovation Scheme to support businesses' innovation activities via enhanced tax deductions/allowances

Tax deduction raised to 400 per cent of qualifying income (from 250 per cent)

For non-profitable companies, to allow them to convert 20 per cent

Dealing with cost pressures

Extend Enterprise Financing Scheme enhancements till 31 March 2024 to facilitate access to credit

Extend Energy Efficiency Grant till 31 March 2024 for SMEs in food services, food manufacturing, and retail sectors to adopt energy-efficient equipment

Integrate training and job placement

Pilot Jobs-Skills Integrators in precision engineering, retail, and wholesale trade sectors to bring together key players to develop industry-relevant training and facilitate job matching

Enhance employment support

Top up S$2.4 billion to Progressive Wage Credit Scheme fund for lower-wage workers, and maintain higher Government co-funding share of eligible wage increases in 2023

Extend Senior Employment Credit and Part-time Re-employment Grant for senior workers till 2025 to continue providing wage offsets, and encourage employers to offer flexible work arrangements and structured career planning

Enhance Enabling Employment Credit to encourage employment of persons with disabilities

Introduce Uplifting Employment Credit to encourage employment of ex-offenders

Building a resilient nation

Steps

Details

Building organisational capabilities

Build organisational capabilities within the public service by putting in place a more comprehensive system to train public servants, mobilise and cross-deploy them for various crisis roles based on their skillsets and expertise

Tap on the capabilities of the private and people sectors in responding to crisis

Ensuring economic and infrastructure resilience

Build up supply chains through diversification of import sources, stockpiling of food and essential items, and local production

Review stockpiling strategies and improve diversification of critical supplies

Design buildings to serve both peacetime and crisis functions

Safeguarding climate resilience

Accelerate low-carbon transition for our economy and society, to achieve net zero emissions by 2050

Take steps to adapt to global warming and rising sea levels

Building resilience among the people

Extend 250 per cent tax deduction for donations to Institutions of a Public Character (IPCs) and eligible institutions to end-2026 to encourage giving

Enhance Corporate Volunteer Scheme to deepen partnerships between businesses and IPCs

Review salary benchmarks and raise salary guidelines for the social service sector

Top up Community Silver Trust by S$1 billion to support social service agencies

Provide a S$10 million top-up to support Self-Help Groups over the next three years

Taxes

Tax type

Details

Corporate income tax

Base Erosion and Profit Shifting Initiative (BEPS 2.0)

Stated intention to implement Global Anti-Base Erosion (GloBE) rules under BEPS Pillar 2 and Domestic Top-up Tax (DTT) for large MNEs from businesses' financial year starting on or after 1 January 2025

This is still subject to review and update

Vehicle tax

Higher marginal Additional Registration Fee (ARF) rates for higher-end and luxury cars

Portion of Open Market Value in excess of S$40,000 and up to S$60,000 will be taxed at 190 per cent; in excess of S$60,000 and up to S$80,000 at 250 per cent; and in excess of S$80,000 at 320 per cent

Cap Preferential ARF (PARF) rebates at S$60,000

Buyer’s Stamp Duty and Additional Conveyance Duties for buyers

Increase Buyer's Stamp Duty (BSD) rates for higher-value properties, with effect from 15 February 2023

For residential properties, the portion of the property value: In excess of S$1.5 million and up to S$3 million will be taxed at 5 per cent (up from 4 per cent); in excess of S$3 million will be taxed at 6 per cent (up from 4 per cent)

For non-residential properties, the portion of the property value: In excess of S$1 million and up to S$1.5 million will be taxed at 4 per cent (up from 3 per cent); in excess of S$1.5 million will be taxed at 5 per cent (up from 3 per cent)

BSD rates on or before 14 February 2023 will apply for eligible transitional cases

Additional Conveyance Duties for buyers, which applies to qualifying acquisitions of equity interest in property holding entities, will be adjusted accordingly

This article shall not be copied, or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

About the authors

Suan Teck Kin

UOB

Suan Teck Kin joined UOB as an economist in 2006. In his current role as Executive Director in Global Economics and Markets Research, he is responsible for macroeconomic and foreign exchange research with a primary focus on China, Hong Kong SAR and Taiwan, and secondary coverage for the ASEAN region. As a member of the Research team, he presents the team’s market views regularly to the Bank’s management team and clients in Singapore and the region.

Teck Kin has more than 10 years of experience in macroeconomics and equity research. Fluent in English and Mandarin, Teck Kin is interviewed frequently by local and international print and broadcast media, as well as financial newswires on the economic and market outlook.

Woei Chen joined UOB as an economist in 2003. She is focused primarily on the Greater China markets including Taiwan, Mainland China and Hong Kong SAR, and South Korea. Her previous coverage areas included various countries in the ASEAN region. Woei Chen regularly shares her views with other business units in the Bank and through the media.

Find out how we can help your business expand across ASEAN. Get in touch

CPI – All Items

The Consumer Price Index (CPI) is commonly used as a measure of consumer price changes in the economy. It tracks the change in prices of a fixed basket of consumption goods and services commonly purchased by the general resident households over time.

The CPI covers only consumption expenditure incurred by resident households. It excludes non-consumption expenditures such as purchases of houses, shares and other financial assets and income taxes, etc.

The CPI – All Items provides a comprehensive overview of the prices of consumer goods and services. Nevertheless, useful information can also be revealed by complementary CPI series derived by excluding specific items in the All Items basket. For example, two other CPI series reported on a monthly basis are the CPI less imputed rentals on owner-occupied accommodation and the MAS Core Inflation.