You are now reading:

ASEAN Consumer Sentiment Study 2025 (Singapore): Cautious spending mirrors dampened sentiments

Find out how we can help you fast-track your investments in the JS-SEZ.

Learn moreyou are in UOB ASEAN Insights![]()

You are now reading:

ASEAN Consumer Sentiment Study 2025 (Singapore): Cautious spending mirrors dampened sentiments

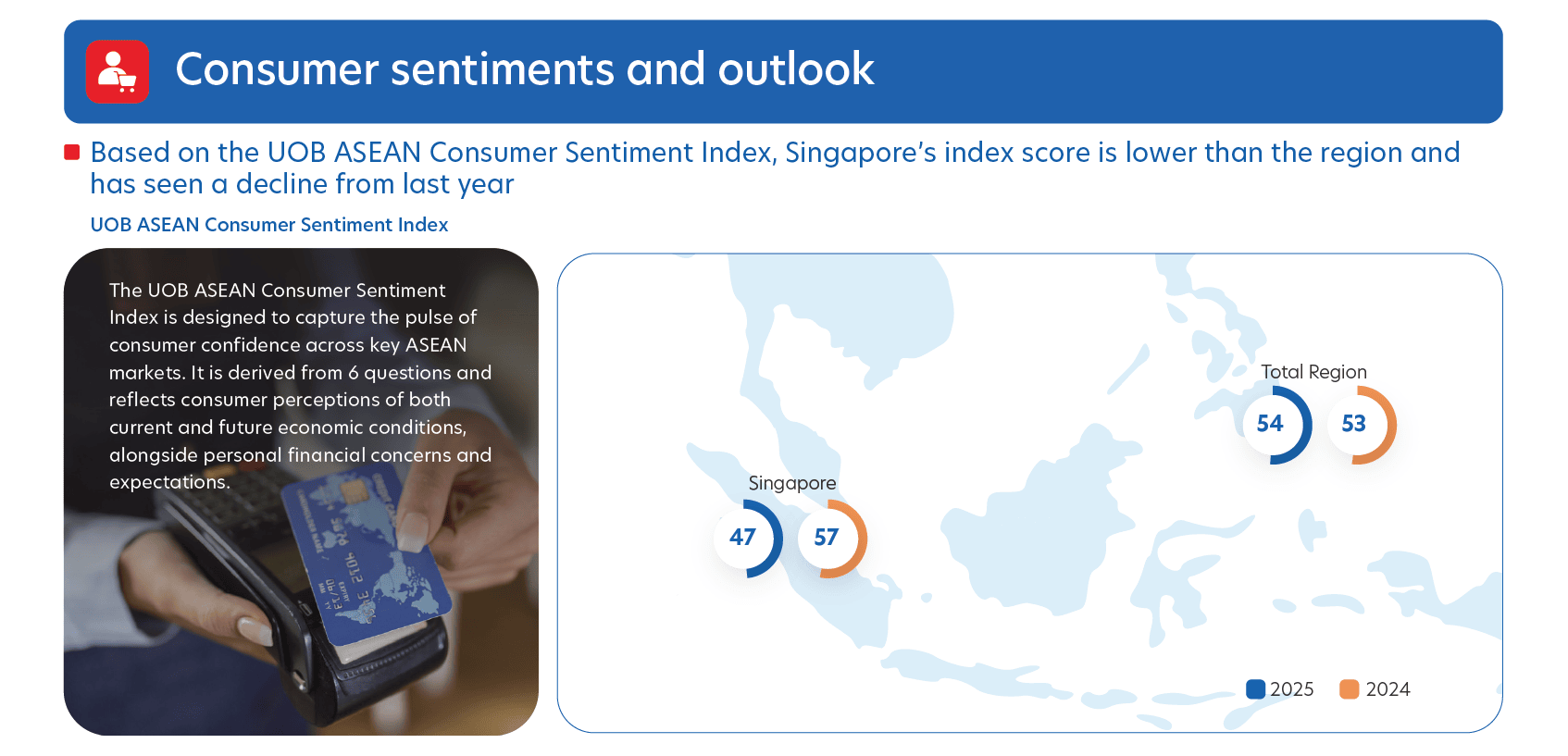

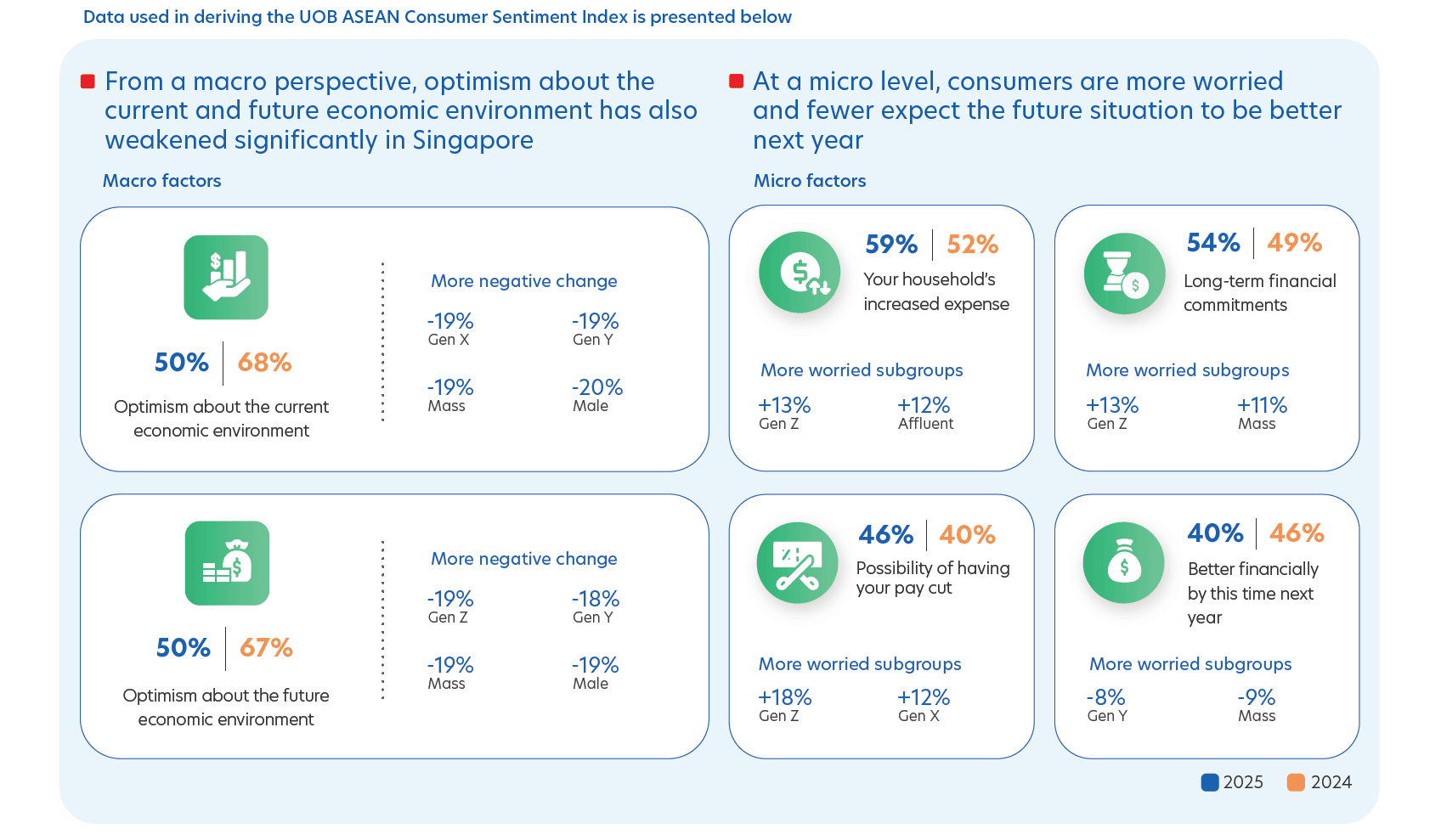

The UOB ASEAN Consumer Sentiment Study 2025 (Singapore Edition) presents in-depth insights from 1,000 consumers spanning various demographic groups. This research study highlights evolving consumer sentiment, spending / financial habits and changes in budget priorities.

Gain a deeper understanding of the factors influencing consumer sentiment in Singapore:

The ASEAN Consumer Sentiment Study (ACSS) is UOB’s regional flagship study analysing consumer trends and sentiments in five countries: Singapore, Malaysia, Thailand, Indonesia and Vietnam. Now in its sixth year, the survey was conducted from May to June 2025 and captures the responses of 5,000 consumers across different demographic groups in the region.

Some of the areas covered include:

This article shall not be copied or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

01 Sep 2025 • 5 MINS READ

15 Jul 2025 • 6 mins read

03 Jul 2025 • 6 mins read