As the Monetary Authority of Singapore offers five new digital banking licences, two Singapore-headquartered banks already have operational digital banks. In March this year, United Overseas Bank launched TMRW, a digital-only, branchless bank in Thailand. TMRW is a completely different offering from UOB Mighty, the bank's digital banking app launched in 2015.

TMRW is revolutionary. Yet, UOB's digital journey was more evolution than revolution, concomitant with its regionalisation strategy, which started as far back as 1999.

In 2010, CEO Wee Ee Cheong realised that UOB needed a common platform to meld together the banks it had acquired in the previous decade, ranging from Radanasin Bank and Bank of Asia in Thailand to Bank Buana in Indonesia and Overseas Union Bank in Singapore. More recently, UOB has expanded in Vietnam. It was the first local bank to be granted a foreign-owned subsidiary bank licence by the State Bank of Vietnam in 2017.

In August this year, UOB opened its second branch in Hanoi. In 2014, UOB was awarded a foreign bank licence by the Central Bank of Myanmar; it opened a full branch in 2015, but is precluded from retail banking.

In further regionalisation initiatives, UOB established its UOB FDI Advisory unit in 2011 to provide companies looking to set up regional operations in Asean with customised banking consultancy services. UOB works with government agencies, business associations and professional service providers to provide these seamless and integrated services.

The integrated regional nature of FDI Advisory made it more imperative to have a common platform across the bank's 500 offices and branches.

Wee was well aware that, despite UOB's local presences in Malaysia, Thailand, Indonesia and Vietnam, it could never have the same level of dominance in those markets as it has in Singapore. As a result, central to UOB's digital strategy is the digital infrastructure for a regional bank.

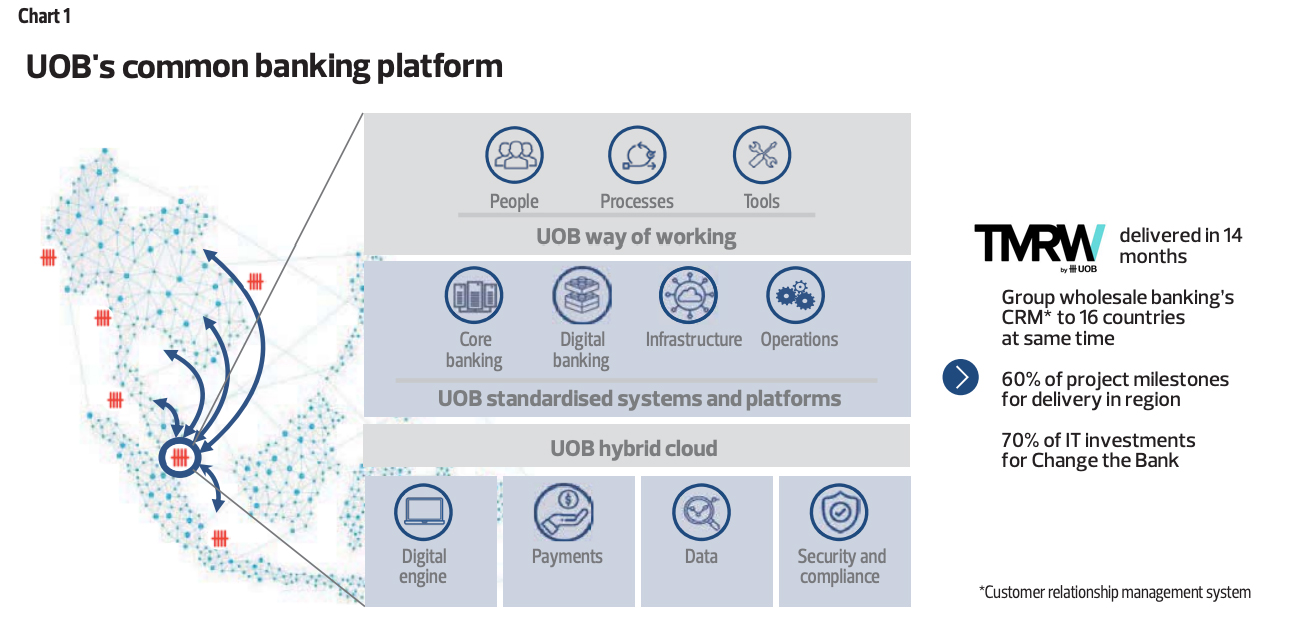

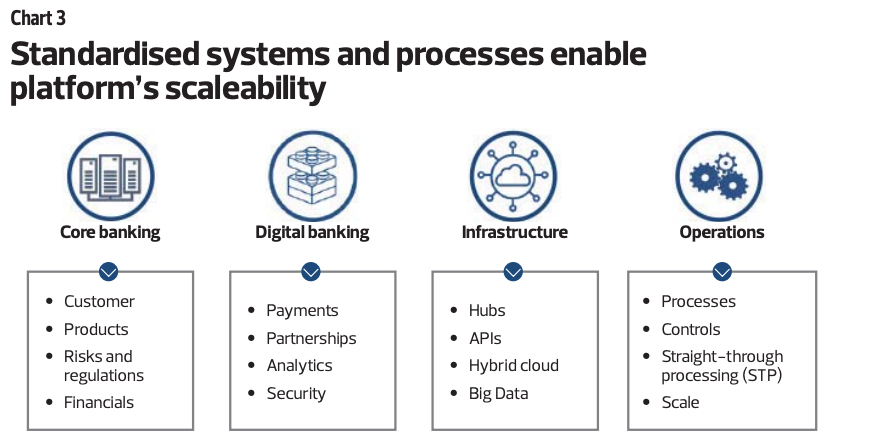

"Having acquired all these banks, our CEO's vision was to take us from being a collection of banks to becoming one regional Asean bank,” says Susan Hwee, Head of Group Technology and Operations at UOB. She started to build the bank's common core banking platform based on the premise of a regional bank more than 10 years ago, realising it had to be modular and scaleable, with products and processes built around the needs of the customer. It is this platform that helped realise Wee's vision of building a seamless Asean bank.

In turn, the common platform helped in serving the expanding regional needs of its customers – both wholesale and retail. In the first six months of the year, UOB's wholesale banking income rose 8% y-o-y to $3.1 billion, underpinned by 9% y-o-y growth in non-Singapore income, 8% y-o-y growth in non-real estate and hospitality income, and 12% y-o-y growth in non-loan income. On Nov 1, it announced in its 3QFY2019 results that around 40% of operating profit of $1.3 billion was from the region.

"Having acquired all these banks, our CEO's vision was to take us from being a collection of banks to becoming one regional Asean bank."

Susan Hwee, Head of Group Technology and Operations at UOB

On UOB's Corporate Day in May this year, it announced a list of goals, including increasing its revenue mix outside of Singapore to around 50%. Even then, UOB is cognisant of the risks of expansion. In an earlier interview, UOB Chief Financial Officer Lee Wai Fai says that, while its Asean footprint will be most important in its growth strategy, the bank needs to control the expansion to maintain its AA rating among the ratings agencies, which is why UOB focuses on improving risk management.

Digital engine

A digital engine, data and security are the three "themes" overlaid on top of the common core banking platform, Hwee explains.

"One of the key things that we then looked at was how to create products and solutions for corporates interested in expanding in the region and to tap intra-Asian investment, capital and wealth flows."

To do this, UOB spent $500 million on infrastructure, starting from a common banking system and overlaying it with the same risk, regulatory framework and financial language across its five geographies. "It took several years of regulatory approvals to be standardised and centralised, so we can have economies of scale," Hwee says of the exercise that was completed in 2014.

New and additional operational and security processes, fintechs and new technologies can be added to UOB's common platform across the region quickly. In 2015, UOB launched UOB Mighty, an all-in-one digital banking app that can do all necessary banking functions for UOB's consumer banking customers. Retail customers can buy shares and gold, place fixed deposits, apply for insurance products, make payments and so on. Other products followed, such as Business Internet Banking Plus (BIBPlus), the digital banking app for UOB's medium-sized companies and large corporates. In 2018, as UOB was readying for TMRW's launch in Thailand, it added artificial intelligence (AI) and machine learning solutions onto the standardised platform to enable the digital bank to process and analyse data to personalise the banking experience for each TMRW customer and keeping its common equity Tier-One capital ratio at 13.7% (as at Sept 30), way above the regulatory minimum.

Making data work

Data management is a large topic in itself. "Just to make data work requires enormous management and dedication," Hwee says. In the beginning – what she calls the first generation of data management – managing data was about getting all the business segments within the bank to share their data to facilitate performance reporting, customer information and risk.

An important use of data management is to enable the banking group to be Basel compliant. The basic Basel rules in 2004 were straightforward. But, then, Basel III and Basel IV required an advanced internal ratings-based (IRB) approach, so UOB had to build a global data warehouse leveraging the standardised core banking systems across the region.

Thus, UOB is able to compute the difference based on regulations in different countries such as foundation IRB for Indonesia and advanced IRB for Singapore. "As we expand outside of Singapore, having the consistent risk lens of Singapore's standard of risk provides a level of comfort and efficiency that is unparalleled," Hwee says.

Collaboration with fintechs

UOB has collaborated with fintechs – either by taking a stake in them, financing or mentorship – to transform the use of its data through TMRW. The bank is also using lessons from TMRW to improve UOB Mighty.

TMRW uses a data categorisation engine by Icelandic fintech, Meniga, to simplify complex and multiple transaction datasets into relevant data for its customers. Meniga's fintech solution is able to sort and categorise large volumes of transaction data. This means customers can match their purchases easily and organise the way in which they manage their finances in realtime, so that it is always personal to them and relevant to their own needs.

UOB has taken a stake in and collaborated with an Israeli fintech, Personetics, which enables TMRW to provide personalised insights based on each customer's different transaction patterns.

The same cognitive analytics engine is also used to drive Mighty Insights, a new service on UOB Mighty that guides customers to stay on top of their financial commitments and goals and to keep track of their expenses.

For credit and risk analysis, UOB is collaborating with Avatec.ai (Avatec), which uses non-traditional data and traditionally available information to determine creditworthiness of an organisation or individual. Avatec was formed in 2018 as a joint venture between UOB and Beijing-based PINTEC Technology Holdings. PINTEC's flagship product is Dumiao, a digital lending solution that uses third-party credit information and e-commerce transactions to generate credit decisions based on AI and machine learning.

With Avatec, banks can now access about 10 times the traditional number of data points used in credit assessments. This means that companies can extend loans to a broader base of customers and at lower loss rates.

Tookitaki, a Singapore-based fintech, and UOB have co-created a machine learning solution that enables its compliance team to conduct deeper and broader analyses as part of its anti-money laundering efforts.

TMRW for Asean's young

TMRW is different from other digital banking and digital bank offerings in Asia, as its business model is focused primarily on deepening customer engagement and growing customer advocates.

Still, was there a need to establish a standalone digital bank, whose delivery is going to be digital-only, with no other touch points, when UOB Mighty was already available in its Asean markets? Hwee says yes.

There is a difference between digital banking and a standalone digital bank. "The young do things differently. Digital banking must serve three generations," Hwee says. UOB's traditional customer base is usually older and wealthier. "Digital banking is omnichannel, which means you serve customers face to face or digitally. It's their choice," she adds. UOB Mighty – as with all banking apps – has an extensive menu. Out of Asean's population of 642.1 million, 50.4% are aged between 20 and 54, according to Aseanstats. At least 94% of Asean's population is literate. Yet, the World Bank estimates that 80% of people in Indonesia, the Philippines, Myanmar and Vietnam, and 30% in Malaysia and Thailand, are unbanked. UOB has an increasing presence in five of these six markets, helped by digitalisation. "The young in Asean are a huge market and we want to be able to serve a new generation of customers," Hwee says.

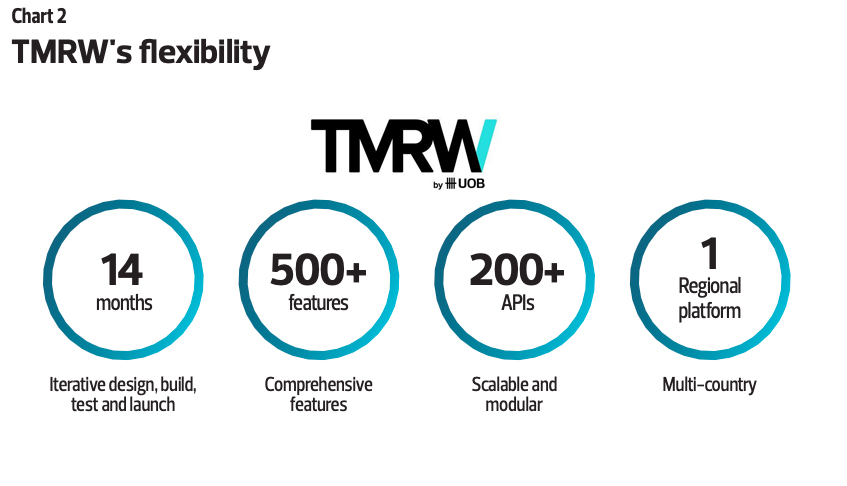

TMRW, which took 14 months to develop, is targeted at young professionals. "We decided there is a need to serve young professionals who are mobile-first. There is a lot [we can learn] from a mobile-first generation, and we want to go somewhere that is larger than Singapore," Hwee says.

A digital bank is a mono-channel strategy in which the bank uses data to engage customers as its primary goal and business model. Interestingly, unlike an omnichannel digital banking app that allows customers to bank on a phone, TMRW has no menu. TMRW is targeted at millennials (those born between 1980 and 1994) and Generation Z (those born in and after 1995). As a digital bank, TMRW is about engagement and not offering higher-yielding deposit accounts and cheap loans.

"We actually spent a lot of time understanding the regulatory framework and the population," Hwee says. TMRW cannot just offer high interest rates [for deposits]. Our measurement is that TMRW's accounts must be properly funded. That means when customers open an account, they must deposit money and not just open accounts for fun with zero balances."

TMRW uses the ATGIE model – acquire customers using AI, transact with a fast digital service, generate data, gain insights with the help of personetics, and create an engagement lab to experiment and learn about engagement.

Net promoter scores, advocates and engagement metrics will be closely monitored. Advocates are customers who have used TMRW and recommend it to their friends. In TMRW's model, NPS reflects customers' sentiment and predicts business growth. The rationale behind a high NPS is that, once customers are happy with TMRW, they will refer the bank to friends. TMRW's target is to have 15% of advocates at the end of the first year.

Most difficult market first

According to a report titled "The Asean Fintech Ecosystem" by Judge Business School, Thailand is the most developed technology market after Singapore. As part of the country's broader Smart Cities and Thailand 4.0 Initiative, the government is aggressively pushing for the development of the fintech ecosystem to transform the country into a fintech hub for the Asean region, the report says.

"Considered one of the more advanced countries in the Asean region after Singapore, Thailand enjoys the second-highest GDP per capita in the region, has a high literacy rate, has more than half of the population living in urban areas and whose median age is 40. The country also possesses the critical digital infrastructure needed for the development of fintech firms; there are 92.3 million mobile phone subscriptions, or a 133% penetration rate, and 57 million internet users, or a 82% penetration rate," the report points out.

Hwee concurs: "The population is digitally very savvy and Thai banks are digitally creative. So, it's a highly competitive market." She is well aware that, as a traditional bank with 155 branches, UOB cannot compete with the local Thai banks. "It's a market we are committed to and in which we have a growing consumer franchise," she says. "If TMRW works in Thailand, we can bring it to a second market within Asean." (CEO Wee has said the next market will be a large market in Asean, which can mean either Indonesia or Vietnam.)

UOB did a lot of groundwork within the Thai regulatory framework of onboarding customers digitally. Thais have digital credentials on their identity cards, and TMRW accounts can be opened in seconds.

"The population is digitally very savvy and Thai banks are digitally creative. So, it's a highly competitive market."

Susan Hwee, Head of Group Technology and Operations at UOB

According to UOB executives, TMRW is not about launching something that anyone can copy; rather, it is about learning from data to engage customers. Based on a survey done by UOB for its launch of TMRW, it found that 60% of Asean's population is below 35, and thus are millennials. TMRW can remind millennials to pay their bills, set aside monies for savings plans at the end of a month. TMRW can also prompt its users with special dining, fitness or other offers depending on their lifestyle. At least 52% of millennials own a smartphone, and they want to bank differently – millennials want a friend, not a bank.

The absence of a fixed menu leaves the bank with the ability to experiment, such as harnessing data to deepen its understanding of each customer so that it can anticipate their needs and serve them accordingly. Whether a customer needs a savings plan or a loan depends on his or her transaction behaviour.

"Barriers to entry for technology are very low. Beyond technology, we have to understand banking and regulations. Banking is about trust, and making money in banking is about risk management; and you have to be profitable to sustain a return to shareholders, which is very important," Hwee says.

Source: The Edge Publishing Pte Ltd. Permission required for reproduction. UOB makes no representation or warranty as to, neither has it independently verified, the accuracy or completeness of the information in this article. Any opinions or predictions reflect the writer’s views as at the date of this article and are subject to change without notice.