UOB bank

June 2019

In the past, telecommunication operators (telcos) used to just be pure utility players focused on building extensive networks and monetising their traditional services by charging for voice, short message system (SMS), international calls and roaming. However, in recent years, over-the-top (OTT) service providers have disrupted the traditional business of telcos by offering communication services through their various applications (apps), resulting in a drop in revenue for telcos’ traditional businesses.

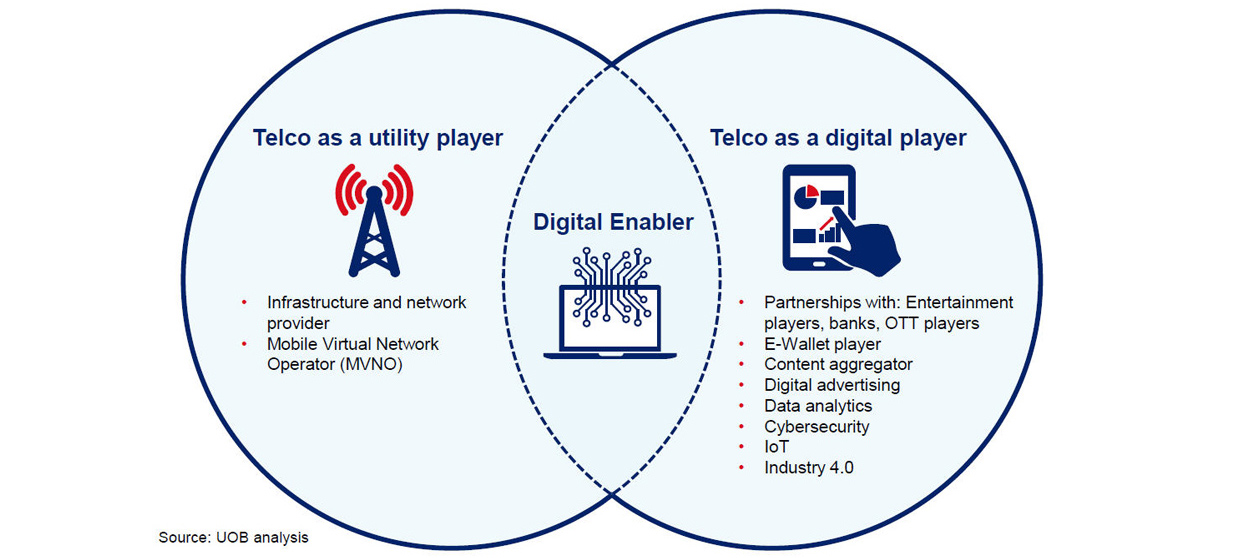

Figure 1 illustrates the evolution in telcos’ business models as they move from being pure utility players to digital players through expansion in the digital space. Most telcos are already “digital enablers” and are continuing to seek new areas of growth to extend their reach across the digital space. We believe it is important for them to do so to remain competitive, especially via increasing services/platforms as that will result in greater stickiness and revenue from consumers. Essentially, as telcos seek to increase their share in the digital space, they need to:

Impact on telco dynamics

Figure 1: Evolving nature of telcos’ business models

Most telcos are trying to streamline their core business and move towards becoming digital players

Connectivity and infrastructure are the core of the telcos’ business. Hence, telcos need to ensure that they are sufficiently advanced in this area to protect their core business before expanding into new business areas.

UOB offers solutions to tackle rising competition within the telecommunications space. For more information on UOB’s value chain solutions for the telecommunications sub-sector, please contact us here.

Click on the button to read the full Industry Perspective.

Download