Singapore: MAS survey upgrades 2021 GDP growth to 5.8 per cent

Economic Outlook

11 Mar 2021

5 mins read

You are now reading:

Singapore: MAS survey upgrades 2021 GDP growth to 5.8 per cent

Key takeaways

In the latest MAS Survey of Professional Forecasters, the median Gross Domestic Product (GDP) outlook for 2021 rose to +5.8 per cent from a previous forecast of +5.5 per cent, with a stronger recovery expected for manufacturing, finance and insurance, and non-oil domestic exports.

However, economic recovery is likely to remain uneven for 2021. The construction, accommodation and food services clusters are expected to contract in the first quarter of 2021.

Inflation risks are expected to remain benign in 2021. The median estimate for headline inflation rose to 0.9 per cent in 2021, up from the previous survey result at 0.6 per cent.

The latest MAS Survey of Professional Forecasters released in March 2021 suggests market-watchers’ continued confidence in Singapore’s recovery momentum. According to the latest report, respondents upgraded their median GDP outlook for 2021 to +5.8 per cent, up from a previous forecast of +5.5 per cent. Growth is also expected to persist in 2022 at +3.8 per cent.

Across sectors, a strong recovery is expected for manufacturing, finance and insurance, and non-oil domestic exports (NODX). The median outlook for Singapore’s manufacturing momentum has been shaded higher to 4.7 per cent in 2021, from December’s outlook of 4.5 per cent. Similarly, finance and insurance is now expected to grow 5.8 per cent in 2021 (up from December’s outlook of 5.1 per cent) while NODX saw a significant upgrade to expand 6.9 per cent for the year ahead (from December’s outlook of 4.0 per cent).

The survey results are in line with our expectations. Our forecast pencils Singapore’s GDP growth at +5.0 per cent and +3.5 per cent for 2021 and 2022 respectively. Growth is expected to be led by manufacturing at +3.0 per cent, services at +3.8 per cent and construction at +41.8 per cent in 2021. This compares to 2020’s performance where the services and construction clusters contracted 6.9 per cent and 35.9 per cent respectively, while manufacturing grew 7.3 per cent.

Note that our construction forecast (+41.8 per cent in 2021) is significantly higher compared to the MAS professional forecaster survey (+22.5 per cent in 2021). This difference may be due to our expectations for construction activities to accelerate on pent-up demand from the slowdown seen in 2020 (-35.9 per cent in 2020). This is also coupled with our view for a relatively controlled COVID-19 situation, which suggests a sustainable return of labour supply to this labour-intensive industry in the months ahead. Overall, the positive growth outlook for Singapore is underpinned by the projected pickup in external demand, coupled with Singapore’s relatively well-controlled COVID-19 situation.

Despite the construction sector’s forecasted growth of +22.5 per cent in 2021 based on the MAS survey, the sector is expected to contract 22.5 per cent year-on-year in the first quarter of this year. Source: Shutterstock

Notwithstanding the recovery for the whole of 2021, the construction and services sectors are expected to contract further in the first quarter of this year. Specifically, the construction sector is expected to contract 22.5 per cent year-on-year in 1Q21, according to the median estimates in the latest professional forecaster survey.

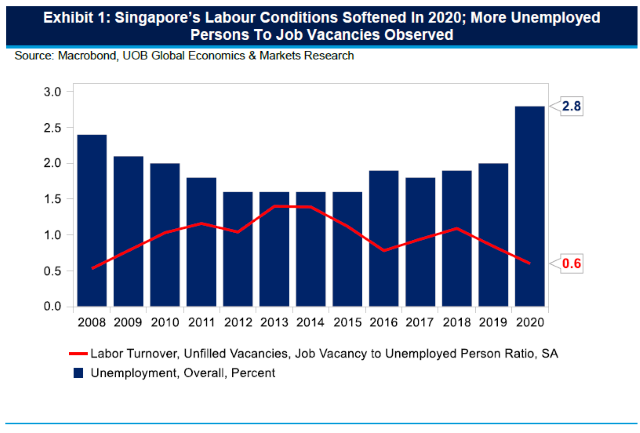

Meanwhile, the accommodation and food services cluster is pencilled to fall 4.5 per cent year-on-year in the same period, suggesting that the respondents remain cautious over the slowdown in Singapore’s international arrivals. Separately, domestic consumption is expected to fall further by 5.0 per cent year-on-year in 1Q21, an unsurprising statistic given the slack in Singapore’s labour conditions seen to-date.

The survey also highlighted three key risks to Singapore’s growth prospects:

COVID-19 concerns topped the list of downside risks, which cited “a further deterioration in the COVID-19 situation, due to new outbreaks or delays in vaccine deployment”.

Geopolitical risks (including US-China tensions) were also mentioned as downside risks to Singapore’s growth momentum.

Respondents were concerned should there be a pre-mature pullback in global macroeconomic policy support.

We have highlighted the above-mentioned risks, specifically that of COVID-19 and geopolitical tensions, in our Singapore Outlook 2021 report.

On the flip side, market-watchers cited several factors that may accelerate Singapore’s economic recovery. These include a faster-than-expected containment of the COVID-19 outbreak, strong manufacturing performance driven by electronics, and the eventual re-opening of borders to international travel.

Beyond COVID-19 related risks, we note that Singapore’s manufacturing industry is likely to remain to be a key growth pillar for 2021. This view is reinforced by the latest Purchasing Managers’ Index (PMI) data, where PMI continued to expand at 50.5 points in February 2021, led by electronics PMI at 50.8.

The survey results also suggested that inflation risks are expected to remain benign in 2021. The median estimate for headline inflation rose to 0.9 per cent in 2021, up from the previous survey result at 0.6 per cent. More importantly, core inflation which is a measure that strips out accommodation and private road transport costs, is pencilled at 0.7 per cent in 2021 (up from previous estimate of 0.6 per cent). Comparing to Singapore’s 20-year long-run headline and core inflation trend at an average of 1.6 per cent between 2000 to 2019, it suggests that inflation risks are far from levels that would be concerning.

In a nutshell, we believe Singapore’s growth outlook for 2021 will depend on three key factors, including (1) how COVID-19 pandemic evolves, (2) geopolitical environment, and (3) global trade dynamics. Uncertainties surrounding COVID-19 and its impact on global (and regional) growth continue to stay elevated to-date. Geopolitical tensions which are seen rising recently in the Taiwan Strait may pose headwinds to economic recovery. Lastly, hopes for US President Joe Biden to take a more constructive and multilateral approach in trade with other countries in addition to the possible ratification of the RCEP agreement towards the end of 2021 could benefit Singapore as a trade-reliant economy.

Important notes and disclaimers

This article shall not be copied, or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

Barnabas Gan

UOB

Barnabas Gan joined the UOB Global Economics and Markets Research team in 2019 and is responsible for providing macroeconomic research focusing on Singapore and India. He provides regular economic commentaries through local and international print and broadcast media

Before joining UOB, he was an economist in a financial institution covering Thailand, Korea and Commodities. He also held research positions in the Prime Minister’s Office of Singapore where he performed risk assessments and horizon scanning roles in relation to policy-making.

Barnabas graduated with a Bachelor of Social Science (Honours) in Economics from the National University of Singapore and also holds a Master of Social Science in Applied Economics from the Singapore Management University.

Find out how we can help your business expand across ASEAN Get in touch