How ASEAN withstood market volatility in 10 charts

Economic Outlook

22 Dec 2022

9 mins read

You are now reading:

How ASEAN withstood market volatility in 10 charts

Key takeaways

Key members in ASEAN have managed to ride through a year of volatile market swings – brought on by global developments such as the lingering pandemic effects, the Russia-Ukraine conflict and rising inflation pressures.

Asian currencies have withstood the onslaught of the USD strength valiantly, while capital flows were orderly and nowhere near the scale experienced during the severe drawdowns in March 2020 when COVID-19 became a global pandemic.

Despite ASEAN’s improved fundamentals, the year ahead is expected to remain challenging with lower GDP growth rates expected globally. However, ongoing recovery in domestic activities and China’s border reopening are expected to offset said decline.

Key members in ASEAN (namely, Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam) have managed to ride through a year of volatility, aided by improved fundamentals.

The year 2022 kicked off with the lingering effects from the COVID-19 Omicron variant, followed by the Russia-Ukraine military conflict which sparked off supply disruptions in the energy and commodity complex. This was followed by a surge in inflation globally and the US Federal Reserve’s aggressive rate hikes to quell inflation pressures.

As US interest rates surged and the USD strengthened, Asian currencies (except for JPY) have held out relatively well, given that the US dollar index (DXY) strengthened as much as 19 per cent at one point. The DXY has since pared about half of its yearly gains.

Through the 10 charts below, this report suggests that several key factors are behind ASEAN’s resilience. These factors are likely to help the region withstand potential volatility in 2023, even as economic recessions in developed markets loom while tightening financial conditions and geopolitical risks linger on.

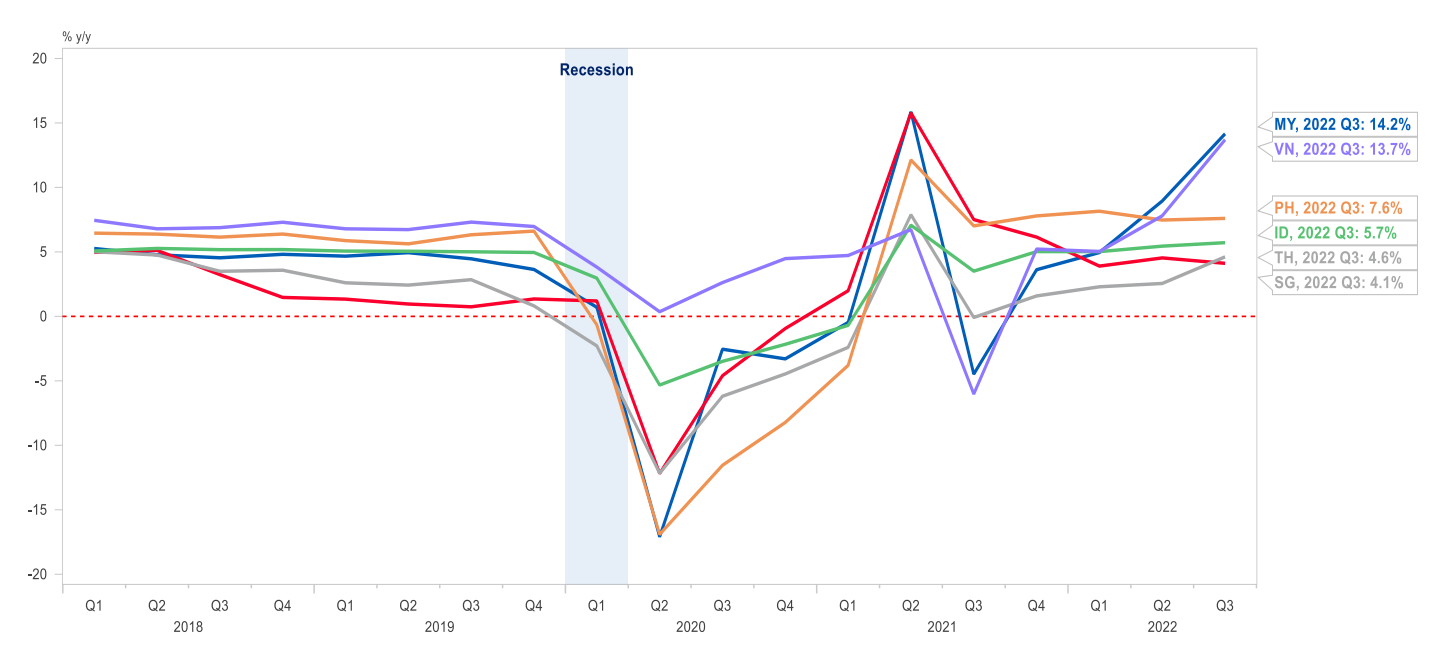

Chart 1: ASEAN’s post-pandemic rebound

ASEAN: Real GDP growth rates (quarterly). Source: Macrobond, UOB Global Economics & Markets Research

GDP growth for most economies has rebounded strongly in 2Q-3Q22 on the back of exports demand and, increasingly, domestic demand as COVID-19 restrictions have mostly been lifted across ASEAN. Malaysia topped the list in 3Q22 with the fastest growth rate in ASEAN.

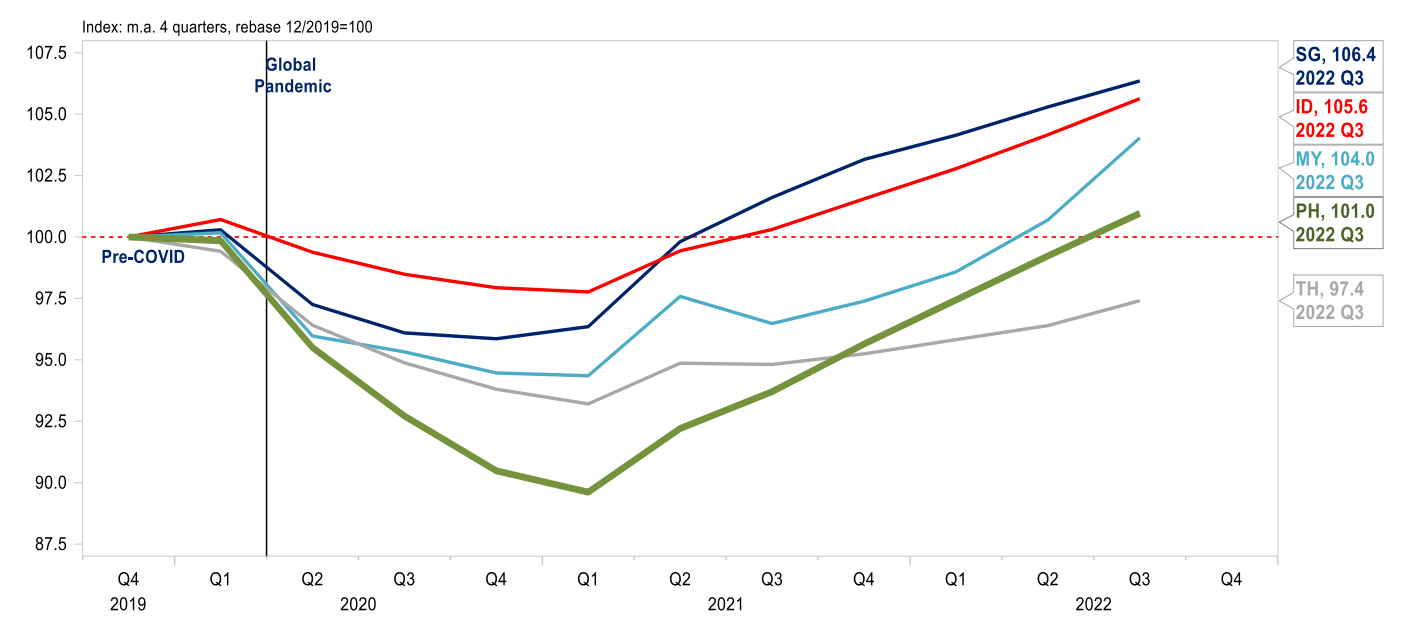

Chart 2: Economic output back on track

ASEAN’s real economic output largely above pre-COVID level. Source: Macrobond, UOB Global Economics & Markets Research

Except for Thailand, national output is now back to pre-COVID levels as ASEAN benefitted from exports demand and reopening of the economies boosted domestic demand. The consistent recovery helps to support income growth and stabilise government finances and financial market confidence, among others.

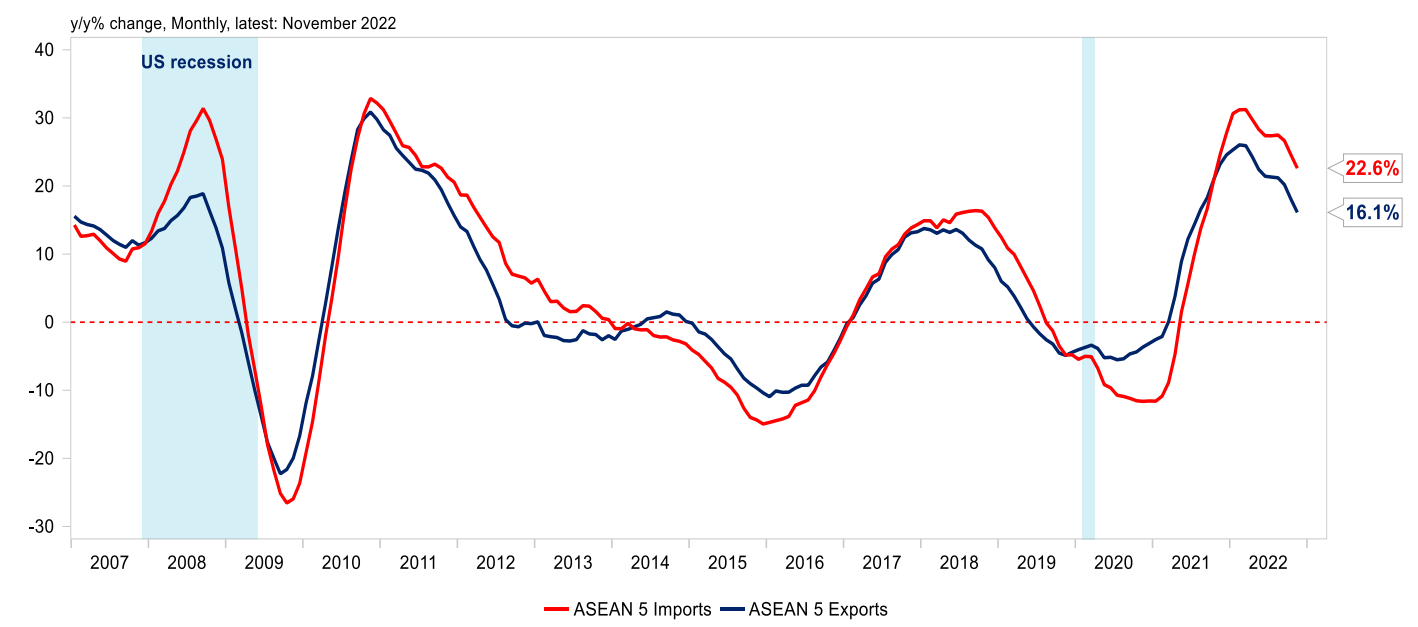

Chart 3: Robust trade performance

ASEAN-5’s trade performance on a 12-month moving average. Source: Macrobond, UOB Global Economics & Markets Research

Exporters and manufacturing sectors in ASEAN were the main beneficiaries especially during the pandemic period, though global demand is expected to soften in the coming months as rising interest rates globally dampen spending and business activities.

Chart 4: Tourism makes a recovery

Inbound visitor arrivals in Asia, YTD. Source: Macrobond, UOB Global Economics & Markets Research

Lifting of COVID-19 restrictions and reopening of domestic economies across ASEAN since mid-2022 added further to recovery momentum as visitor flows surged and services sectors rebounded. These factors are expected to be the main pillar for various ASEAN economies in 2023. As and when China further relaxes its zero-COVID policy and reopens its borders, it will be a further boost to the tourism-related sectors across ASEAN.

Chart 5: Benign inflation

Selected economies’ inflation rate – historic and forecasts from International Monetary Fund (IMF). Source: Macrobond, UOB Global Economics & Markets Research

Inflation rates in Asia and ASEAN have generally been at lower levels relative to the developed markets in 2022, as consumer prices are partially cushioned by administrative measures as well as access to energy, mineral and agriculture commodities for some ASEAN countries. This means that regional central banks’ policy tightening is less aggressive than the Fed’s, allowing more flexibility for economic expansion.

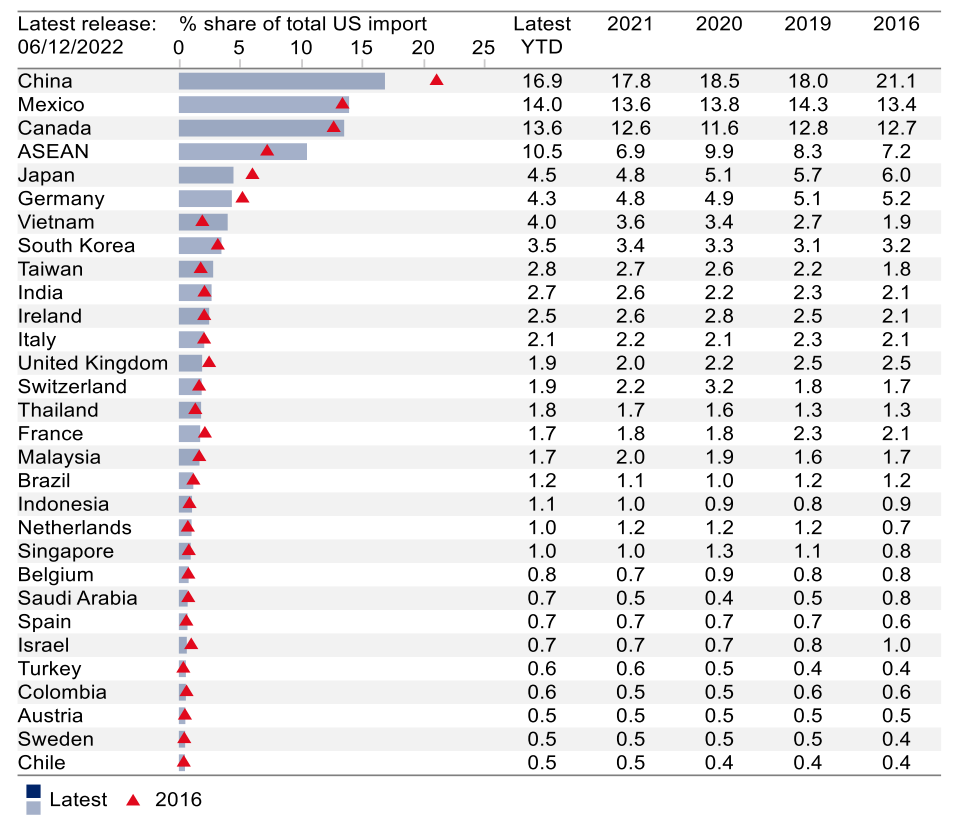

Chart 6: Supply chain shifts

United States: Top import sources, YTD (percentage share). Source: Macrobond, UOB Global Economics & Markets Research

This is reflected in the share of US’ imports from ASEAN, particularly Vietnam, while US’ imports from China fell after 2016 when Trump became US President and US-China tensions flared up. The shifts are likely to be structural with US pursuing various measures to counter China’s rise, including onshoring, offshoring and “friendshoring”, and deglobalisation/regionalisation of supply chains, all of which will benefit ASEAN as a manufacturing and exports hub.

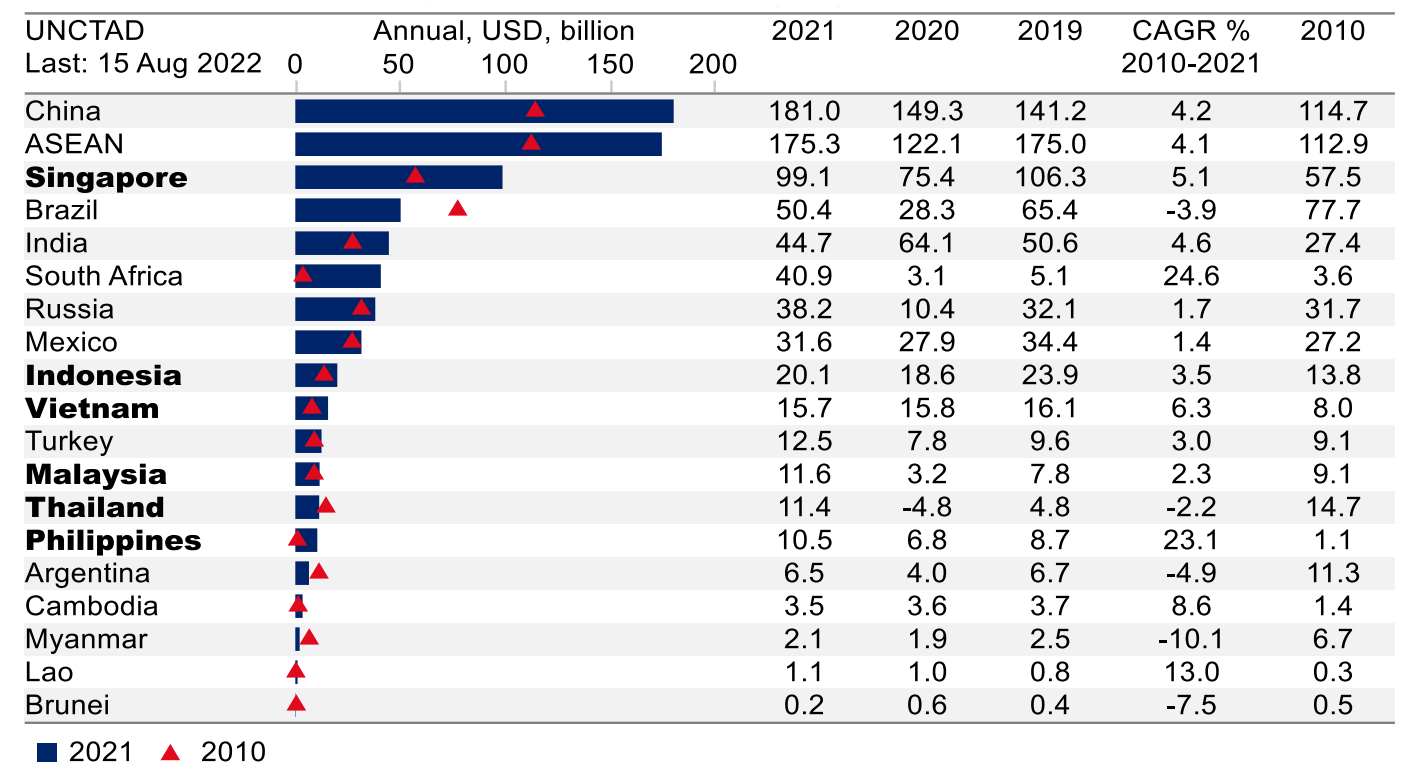

Chart 7: Healthy investment inflows

Foreign direct investment (FDI), inward flows. Source: Macrobond, UOB Global Economics & Markets Research

Supply chain shifts are also accompanied by investment inflows, leading to a surge of FDI inflows to the region as businesses set up manufacturing plants, warehouse facilities, distribution networks, and others. Despite the pandemic conditions, FDI inflows to ASEAN jumped by 44 per cent in 2021 to a new record high of US$175.3bn, above the previous record set in 2019. ASEAN is also the world’s third largest destination of FDI inflows, after the US and China.

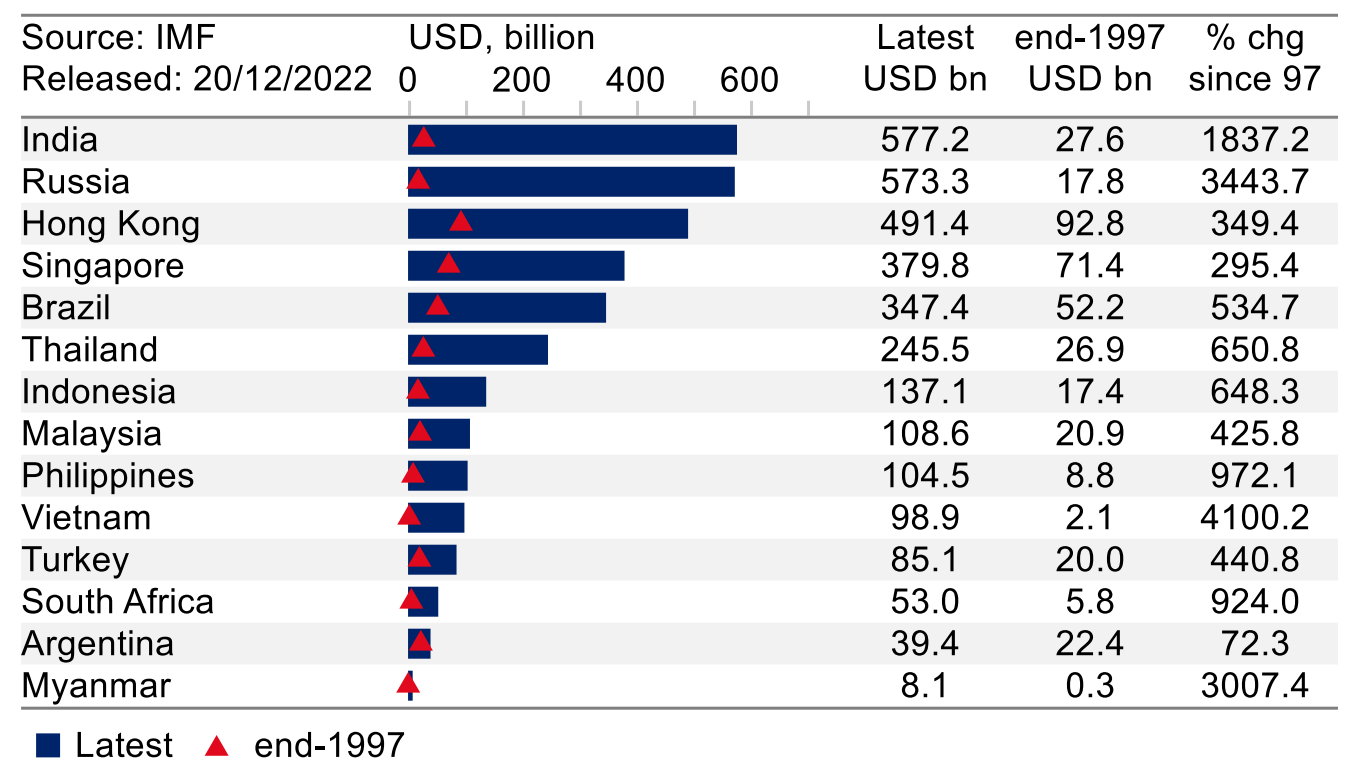

Chart 8: Ample foreign reserves

IMF International Financial Statistics (IFS) – official reserve assets in USD. Source: Macrobond, UOB Global Economics & Markets Research

The build-up in foreign reserves since the Asian financial crisis has allowed for greater buffer against financial market volatility. Despite the depletion over the past 12 months in view of the strong US dollar, the quantum of reserves on hands remains substantial compared to the levels seen in 1997. These will continue to serve as a buffer against sharp capital outflows from domestic markets.

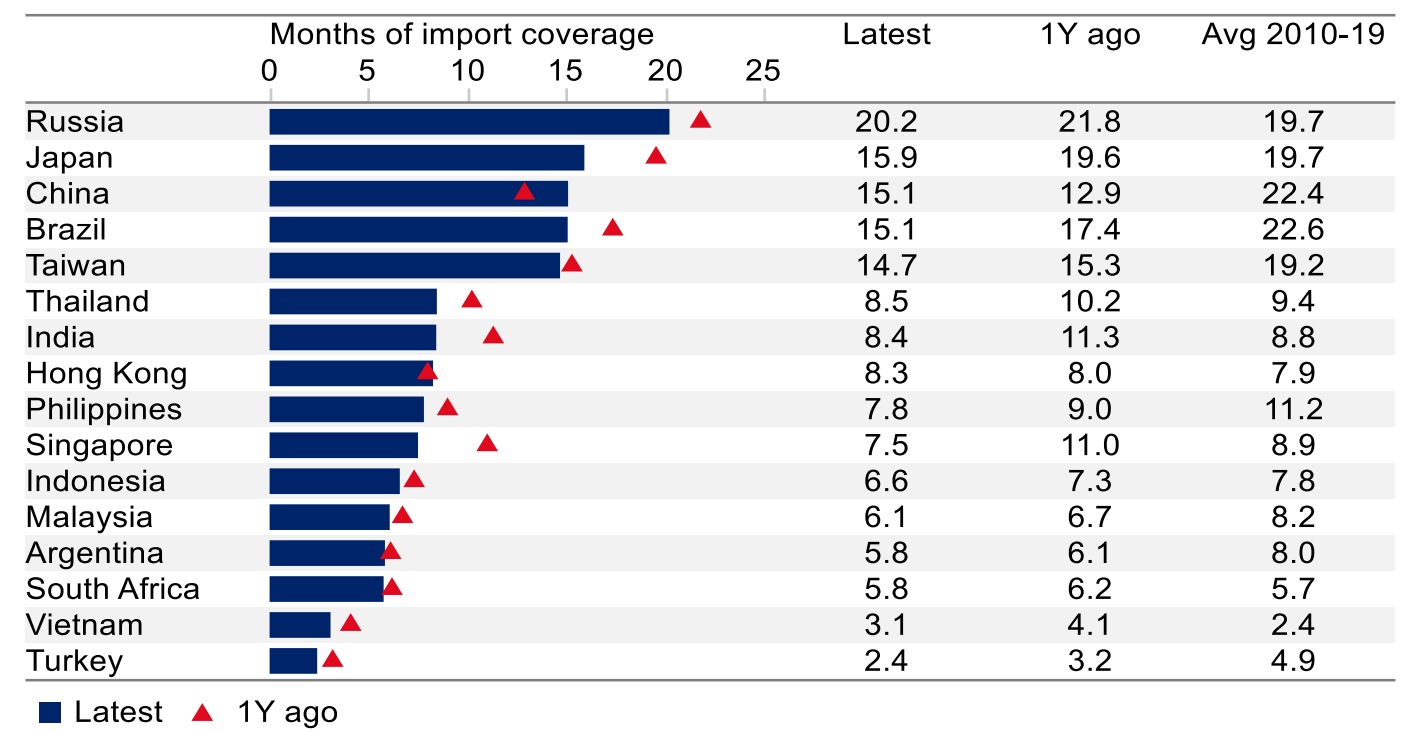

Chart 9: Ability to pay imports

International reserves: Months of imports coverage. Source: Macrobond, UOB Global Economics & Markets Research

The ability to pay for imports is another test of confidence and most of the ASEAN countries have more than sufficient reserves available to pay for 3 months of imports (which is seen as an international “rule of thumb”).

Chart 10: Minimal short-term external debt

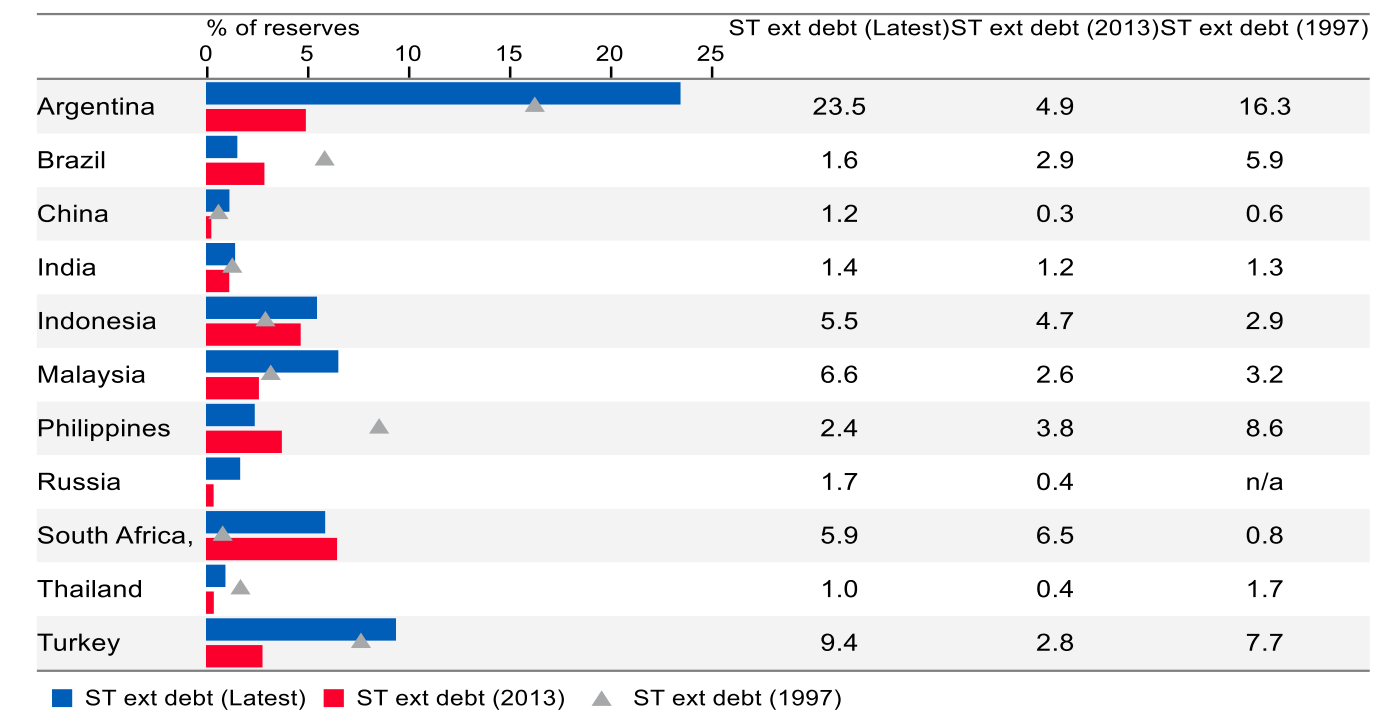

Ratio of short-term external debt to FX reserves (%) – comparisons. Source: Macrobond, UOB Global Economics & Markets Research

Most of the ASEAN countries have relatively small amounts of short-term external debt in proportion to their reserves, except for Indonesia and Malaysia, which are still below 10 per cent of their foreign reserves. This keeps ASEAN countries in a good position to withstand the pressures of a strengthening USD and rising global interest rates.

Outlook – Slower growth pace in 2023

While improved fundamentals have allowed ASEAN markets to withstand the financial market volatility in 2022, the year ahead is expected to remain uncertain and challenging amid looming risks of economic recessions in the US and Europe, tightening financial conditions, further straining of US-China relations and Russia-Ukraine conflict, among others. Given the export-oriented nature of ASEAN economies and the world’s third largest destination of FDI inflows, the possibility of spillovers from these risk factors cannot be ignored.

However, these are offset somewhat by the ongoing recovery in domestic activities with the relaxation of COVID-19 pandemic restrictions and reopening of cross border movements, which will benefit domestic oriented sectors such as retail, food and beverage, transport, accommodation, among others. One potential uplift will be when China reopens its borders, which will revitalise the tourism sector especially for Thailand, Malaysia, Singapore and Vietnam.

Overall, GDP growth rates around the world will be lower in 2023 with developed markets such as the US, Europe and UK experiencing full year declines, while the main economies in ASEAN are expected to see growth rate slowing to sub-5 per cent pace in 2023 from above 6 per cent in 2022. China will likely see meaningful recovery in 2023 as we anticipate further gradual easing of its COVID-19 measures next year (which may quicken as the government plans to accelerate elderly vaccination) as well as the flow-through of stimulus measures.

This article shall not be copied, or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

Suan Teck Kin

UOB

Teck Kin joined UOB as an economist in 2006. In his current role as Executive Director in Global Economics and Markets Research, he is responsible for macroeconomic and foreign exchange research with a primary focus on China, Hong Kong and Taiwan, and secondary coverage for the ASEAN region. As a member of the Research team, he presents the team’s market views regularly to the Bank’s management team and clients in Singapore and the region.

Find out how we can help your business expand across ASEAN Get in touch