This is the first article in a six-part series exploring findings from the FinTech in ASEAN 2021 research. It looks at consumers’ digital financial adoption in Indonesia.

Download FinTech in ASEAN 2021

Key takeaways

- Indonesia’s FinTech ecosystem is the largest in the ASEAN region based on the number of users.

- One in three Indonesians use e-wallets as their default mode of payment, the highest proportion in ASEAN.

- E-wallets are favoured for their convenience, though a breakaway winner is yet to emerge in Indonesia’s e-wallet ecosystem.

- Low credit penetration opens up an opportunity for continued buy now, pay later (BNPL) growth.

- The rapid influx of novice investors in Indonesia demands more care from regulators.

According to the e-Conomy SEA 2021 report1, nearly three-fourths of Indonesia's 21 million new digital consumers since the pandemic hail from non-metropolitan areas. These consumers comprise a thriving and eager market for the FinTechs, startups and firms that have set their long-term sights on the country.

The growth of digital-first financial services such as micro-insurance, on-demand buy now, pay later (BNPL), and online investments is fuelled by the strategic partnerships between pure-play startups, banks and ever-expanding e-commerce giants. In 2021, e-commerce remained the main growth driver of the nation's internet economy; according to the same report, eight in 10 Indonesian internet users made at least one purchase online.

In UOB's FinTech in ASEAN 2021 report, produced in collaboration with PwC Singapore and the Singapore FinTech Association, we examined the impact of the 'surge to digital' on FinTechs, FinTech investors and consumers in ASEAN-6 countries — Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam. Our consumer survey2 results paint a clear picture of Indonesia's bright FinTech future.

Digital payments are overwhelmingly driven by convenience

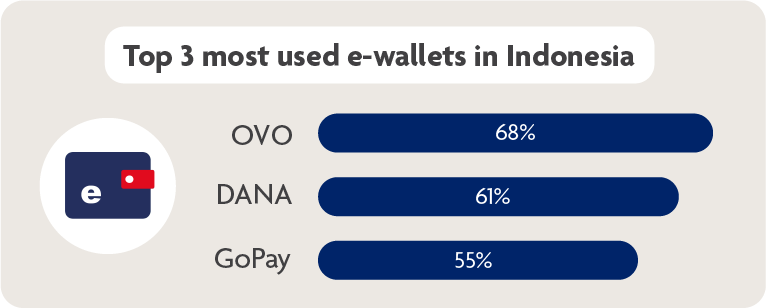

Figure 1: The three most used e-wallets in Indonesia are locked in a close race, with no clear winner yet3. Source: FinTech in ASEAN 2021 research

OVO, DANA and GoPay reign in Indonesia, where cashless digital payments are becoming the standard to facilitate increased activity in digital services like e-commerce, ride-hailing and food delivery. OVO, jointly-owned by conglomerate Lippo Group and Grab, is the ride-hailing giant's alternative to GrabPay in Indonesia. OVO and GoPay are used to facilitate transactions in their respective apps (ride hailing and food delivery) and by partnering offline merchants. Both apps are integrated with Tokopedia, one of the nation's largest e-commerce platforms.

DANA, on the other hand, was a relatively late entry to the game. Founded in December 2018, the e-wallet is majority-owned by local media giant EMTEK and is often used to facilitate online bill payments for necessities such as electricity and mobile data.

When asked about their most used payment method, 33 per cent of Indonesian respondents voted for e-wallets4, making it the second-most popular option after cash. However, unlike the rest of the ASEAN-6, Indonesia has no breakaway favourite for e-wallets. Indonesians use multiple e-wallets to transact, and the battle for dominance hinges on the e-commerce sector, which recorded 52 per cent year-on-year growth, according to the e-Conomy SEA 2021 report.

Which of these payment methods do you use most often?

| Payment method | Indonesia | ASEAN-6 |

| Cash | 46% | 38% |

| Debit/Credit cards | 7% | 20% |

| E-wallets | 33% | 20% |

| Mobile banking apps | 7% | 12% |

| E-commerce payment platforms | 7% | 6% |

Table 1: Payment methods most frequently used by respondents in Indonesia vs. ASEAN-6. Source: FinTech in ASEAN 2021 research

These apps are favoured for their convenience (82 per cent), the ability to earn rewards/loyalty points (50 per cent), and the opportunity for cash rebates (47 per cent)5. Most QR-based digital wallets have also been integrated with PeduliLindungi, Indonesia's national COVID-19 contact-tracing database, which means they can be used to check in to physical venues.

Explore the data | Payment preferences of ASEAN consumers

New retail investors need appropriate support

Just as TikTok cooking, dalgona coffee and affordable home improvement ideas captivated Indonesian consumers during the pandemic, so too did retail investments. During lockdown measures, many working adults, particularly millennials, embraced the opportunity to learn about investments from home6. The number of retail investors in Indonesia grew 90 per cent between December 2020 and December 20217.

The pandemic offered people the opportunity to explore new passions and hobbies, including stocks. Photo: Afif Kusuma/Unsplash

The pandemic offered people the opportunity to explore new passions and hobbies, including stocks. Photo: Afif Kusuma/Unsplash

Indonesian retail investors, who have invested through digital trading and wealth management platforms, mainly do so via traditional online brokerage platforms, online-only trading platforms, cryptocurrency exchanges and non-bank robo-advisors (see Table 2). Survey respondents in Indonesia were also much more likely to use non-bank robo-advisors than those backed by established financial institutions; this could be due to the lack of banks offering integrated robo-advisory functions within their banking apps in the first place.

Have you invested using digital trading and wealth management platforms? If yes, which are the types of platforms that you have invested your funds in?

| Type of digital investment platform | Indonesia | ASEAN-6 |

| Traditional online brokerage platforms | 25% | 31% |

| Online-only trading platforms | 24% | 22% |

| Cryptocurrency exchanges | 23% | 27% |

| Financial institution-backed robo-advisors | 8% | 14% |

| Non-bank robo-advisors | 24% | 16% |

| Micro-savings cum investment platforms | 9% | 13% |

| Have not invested using digital assets and wealth management platforms | 45% | 41% |

Table 2: Digital investing platforms used by respondents in Indonesia vs. ASEAN-6. Source: FinTech in ASEAN 2021 research

Low financial literacy has resulted in unfortunate scenarios like the Bukalapak IPO in August—as the company’s shares tumbled below the initial 850 rupiah price, novice investors bombarded Bukalapak’s App Store and Play Store pages with 1-star reviews8 to vent their frustrations. Financial regulators like OJK, investment platforms and finance influencers need to concentrate their efforts towards educating new investors of the myriad risks associated with online investments and build more informational resources into their services.

Explore the data | How ASEAN consumers are investing

Crypto force in the making

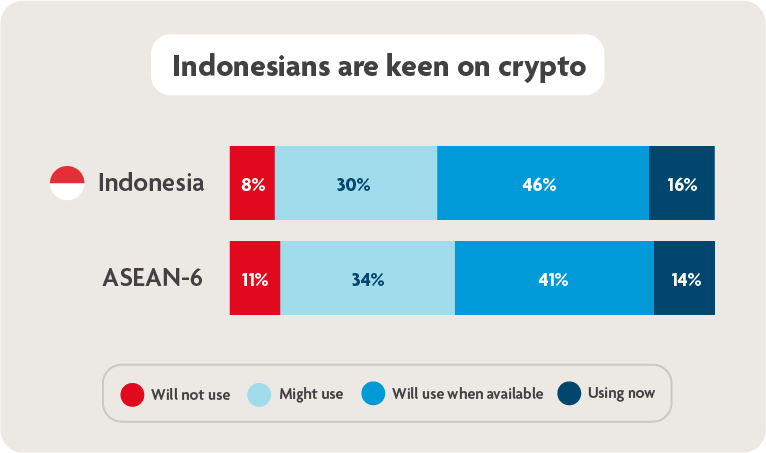

Figure 2: More than half of Indonesian respondents are using or are willing to use digital currencies. Source: FinTech in ASEAN 2021 research

With one of the largest populations in the world, Indonesia could be a crypto force in the future: more Indonesians invest in cryptocurrencies than traditional stocks, according to Indonesia's Ministry of Trade9. Cryptocurrency trading platform Indodax, formerly bitcoin.co.id, is said to be one of the most popular platforms10 for retail investors.

Many consumers in Indonesia are open to using digital currencies—16 per cent already do, and another 46 per cent are interested11 but weren't currently using digital currency at the time of UOB's survey. Still, the road to widespread adoption may not be entirely smooth. In November 2021, Majelis Ulama Indonesia (the nation's top body of Islamic scholars) released a fatwa claiming that cryptocurrencies are illegal under Islamic law. The group later clarified that cryptocurrencies would be tolerated as investment instruments, but unapproved as a medium of exchange due to its volatile nature.

Indonesian survey respondents stated that they would be enticed to use digital currencies such as cryptocurrencies and central bank digital currencies (CBDC) if they saw growing acceptance by established corporations (62 per cent) and had proof that transactions were private (62 per cent)12. To counteract concerns associated with unregulated cryptocurrencies, the nation's central bank has reportedly been considering the release of its own CBDC13.

Low credit card penetration makes way for digital lending and BNPL

Consumer Google search interest for BNPL grew sixteenfold in ASEAN this year, said the e-Conomy SEA 2021 report. Indonesia’s high portion of underbanked consumers and low credit card penetration provide a sterling opportunity for platforms like ShopeePayLater, GoPayLater, Kredivo and Akulaku, all of which offer loans at the point of sale.

The convergence of e-wallets, e-commerce platforms and BNPL has made it possible for consumers to bypass traditional banking ecosystems. The relative ease and growing availability of BNPL platforms make Indonesians far more interested in BNPL (42 per cent) for future purchases than credit card instalment plans (25 per cent).

Some retailers offer the option of pay later plans for purchases (electronics, fashion items, etc). Which pay later methods have you used or intend to use?

| Pay later method | Indonesia | ASEAN-6 |

| Credit card instalment plans | 25% | 47% |

| Buy now, pay later schemes (i.e. Atome) | 42% | 31% |

| I prefer to pay upfront | 44% | 35% |

Table 3: Indonesians are more interested in BNPL schemes compared with the ASEAN-6 average, where preference is for credit card instalment plans. Source: FinTech in ASEAN 2021 research

Indonesians would be most encouraged to try BNPL schemes because of sign-up promotions and promotion referrals (51 per cent), competitive interest rates compared to credit cards (51 per cent), and because they do not have credit cards (28 per cent)14 . Not only do consumer-facing BNPL services promise highly competitive zero per cent interest loans—applicants can be approved in less than an hour with just a selfie.

Human touch is irreplaceable for Indonesians making insurance decisions

Micro-insurance is growing in Indonesia15. Besides microcredit life insurance, micro-insurance has been available in these four basic areas: personal accident, term life, home fire, and business interruption insurance. Through digital tools and platforms, insurers can reach more consumers or serve them better. However, it will still take time to offer comprehensive coverage for Indonesia’s large population—69 per cent of respondents16 stated that they have not purchased insurance online before.

The recent spotlight on health and wellbeing has spurred interest in online life and health insurance, as pictured in this photo of cyclists in Jakarta. Photo: Gema Saputera/Unsplash

The recent spotlight on health and wellbeing has spurred interest in online life and health insurance, as pictured in this photo of cyclists in Jakarta. Photo: Gema Saputera/Unsplash

Insurance products may not be as straightforward or simple as other consumer services, and its advantages are not as obvious immediately. Therefore, the human touch remains highly relevant in this market. Of those who have not purchased insurance online before, 70 per cent would prefer speaking to an insurance professional to make an informed choice; 31 per cent of respondents are also apprehensive about the possibility they would have to do their own claims processing17.

Despite the hesitance, growth will accelerate in this sector as the travel industry recovers, consumers make more big-ticket purchases online and education about the importance of insurance becomes more widely available in the pandemic. E-commerce platforms like Tokopedia and Shopee have begun offering micro-insurance as an add-on during the checkout process for a nominal fee (in most cases, less than Rp. 50.000, or under US$3.50). In our research, almost one in two Indonesians (45 per cent) have bought parcel delivery insurance for their online shopping purchases before, significantly higher than the regional average (23 per cent)18.

Digital banks need to offer interesting experiences and competitive promotions

In the last two years, incumbents and new market entrants to digital banking launched within months of each other: TMRW by UOB, Bank Jago and Neo Bank, to name a few. It is an exciting space, and just seven per cent of respondents said they would not be interested in a digital bank account. Over half of respondents are interested (58 per cent), and 35 per cent are opting for a wait-and-see approach19. Over half of consumers (54 per cent) expressed that new, engaging experiences and competitive rates and promotions are key to winning them over20.

TMRW by UOB offers a hyper-personalised digital banking experience for retail consumers. Photo: UOB

TMRW by UOB offers a hyper-personalised digital banking experience for retail consumers. Photo: UOB

Indonesians are curious and open to trying new things; honing the customer experience to create value is the most immediate way to improve stickiness. For a majority of FinTechs in the ASEAN region, the country will be a most exciting and valuable market to watch.

For more insights on Indonesia and ASEAN's dynamic FinTech industry, please download FinTech in ASEAN 2021: Digital takes flight.

1e-Conomy SEA 2021 report by Google, Temasek and Bain & Company

2An electronic survey was conducted from 25 August to 7 September 2021 with a total of 3,086 respondents across Indonesia (519), Malaysia (513), the Philippines (512), Singapore (508), Thailand (515) and Vietnam (519) to find out more about their digital financial behaviours.

3FinTech in ASEAN 2021 research question A3: Which e-wallet(s) do you use most regularly, if any? Base: Total respondents

4Question A1_2: Thinking about your shopping habits, which of the following payment methods have you used the most often? Base: Total respondents

5Question A2: What are the factors that influence your choice of paying via a digital payment method? Base: Total respondents

6Millennial generation, the main factor increasing retail investors in the capital market, Universitas Gadjah Mada Faculty of Economics and Business News, 14 October 2021

7Indonesian portfolio investors grow at five-year high in 2021, The Jakarta Post article, 24 December 2021

8Novice investors in Indonesia get burned by frequent IPO reversals, DealStreetAsia article, October 2021

9Indonesia now has more crypto investors than stock market investors, The Jakarta Post article, 6 August 2021

10Indonesia considers plan to tax trade in cryptocurrencies, Reuters article, 11 May 2021

11Question A7_1: A growing number of merchants worldwide are starting to accept digital currencies [like cryptocurrencies and central bank-issued digital currencies] as a mode of payment. Given a choice, would you use a digital currency? Base: Total respondents

12Question A7_3: Why would you want to use a digital currency? Base: Those who would use a digital currency

13Bank Indonesia Mulls Digital Currency as a Way to ‘Fight’ Crypto, Bloomberg article, 30 November 2021

14Question B7: What are some reasons why you have chosen or may choose to use BNPL schemes? Base: Those who have used or intend to use pay later methods

15Insurance in Indonesia - Opportunities in a dynamic market, Page 27, KPMG, April 2016

16Question C1: Have you purchased any insurance online before? Base: Total respondents

17Question C3: What are the reasons holding you back from purchasing insurance online? Base: Those who have not purchased insurance online before

18Question C5: Which of these insurance products have you purchased before, or are interested to purchase? Base: Total respondents

19Question E2: With the increase in digital-only banks across Asia, would you consider banking with a digital bank? Base: Total respondents

20Question E3A: What are the factors that would make you want to open a bank account with them? Base: Those who considered banking with a digital bank