ASEAN: FDI inflows declined in 2020 but RCEP to be the next impetus

Trade & Investments

29 Jan 2021

8 mins read

You are now reading:

ASEAN: FDI inflows declined in 2020 but RCEP to be the next impetus

Key takeaways

Global foreign direct investment (FDI) flows declined by 42 per cent in 2020 with ASEAN recording a more moderate fall of 31 per cent.

China became the top FDI destination after its decisive handling of the pandemic and early economic recovery, while the US fell to second position.

FDI is expected to remain weak in 2021, although historically, ASEAN has generally outperformed the competition for FDI inflows, due to stability in the region, and an openness to foreign investments.

RCEP will be another catalyst for ASEAN’s prospects ahead. RCEP countries have been the leading destinations for global FDI inflows in recent years, and this position is likely to be entrenched further once the FTA comes into force.

The region’s global value chain (GVC) participation, China’s dual circulation strategy and ASEAN’s rising population and income will also be the main drivers for further investments into the region.

FDI into ASEAN fell sharply in 2020 amidst global pandemic

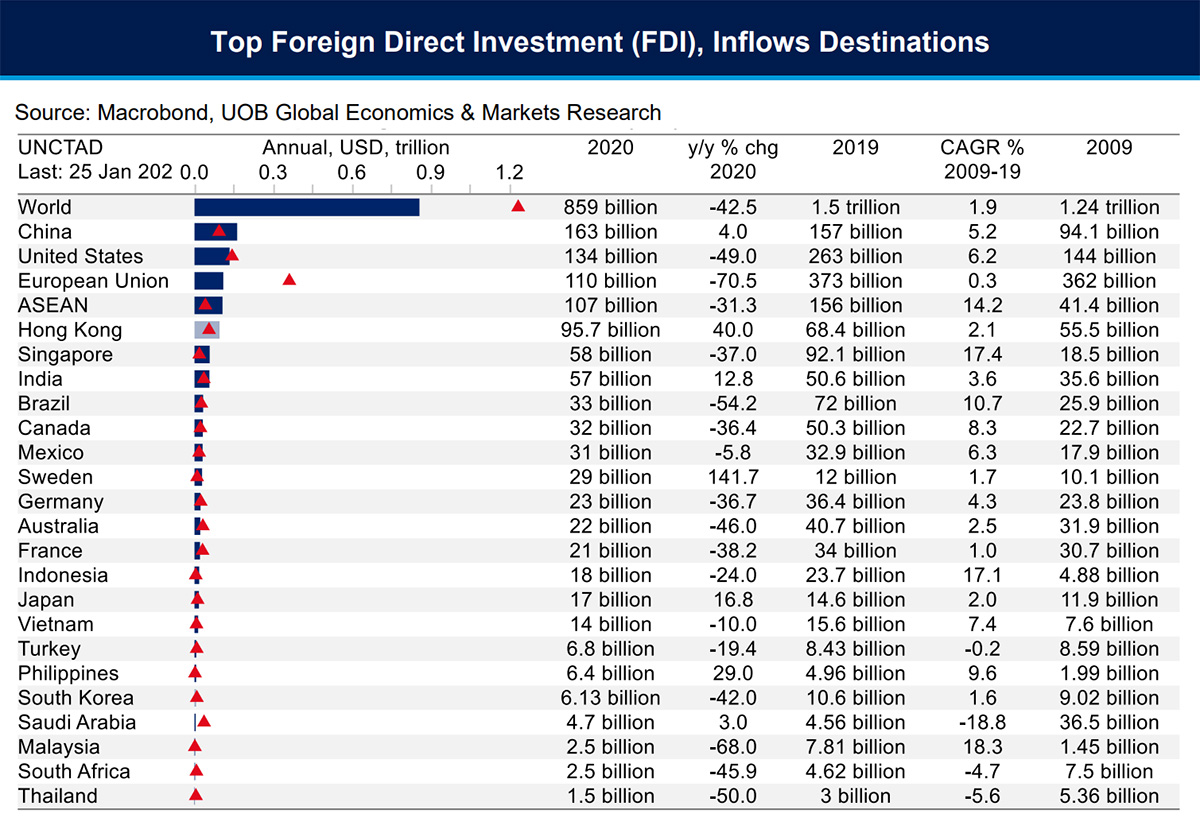

Latest data released by UNCTAD (United Nations Conference on Trade and Development) showed that foreign direct investment (FDI) inflows into ASEAN declined 31 per cent to US$107 billion in 2020.

However, the drop in ASEAN was relatively less severe than the global FDI flows which fell 42 per cent during the year, as the COVID-19 pandemic impacted all types of investment channels: greenfield investment projects, cross-border M&As, and international finance project deals.

Notably, FDI inflows to China rose four per cent to US$163 billion in 2020, along with an increase of inflows into Hong Kong SAR as well, despite the twin impact from the aftermath of the 2019 unrest and the global COVID-19 pandemic faced by the city.

China thus became the top destination of FDI inflows in 2020, with the US trailing in second position after a 49 per cent drop in inflows. This was followed in third place by the European Union, which saw an outsized 71 per cent decline in FDI inflows.

Figure 1: Top FDI recipients in 2020

Differing performance among ASEAN members

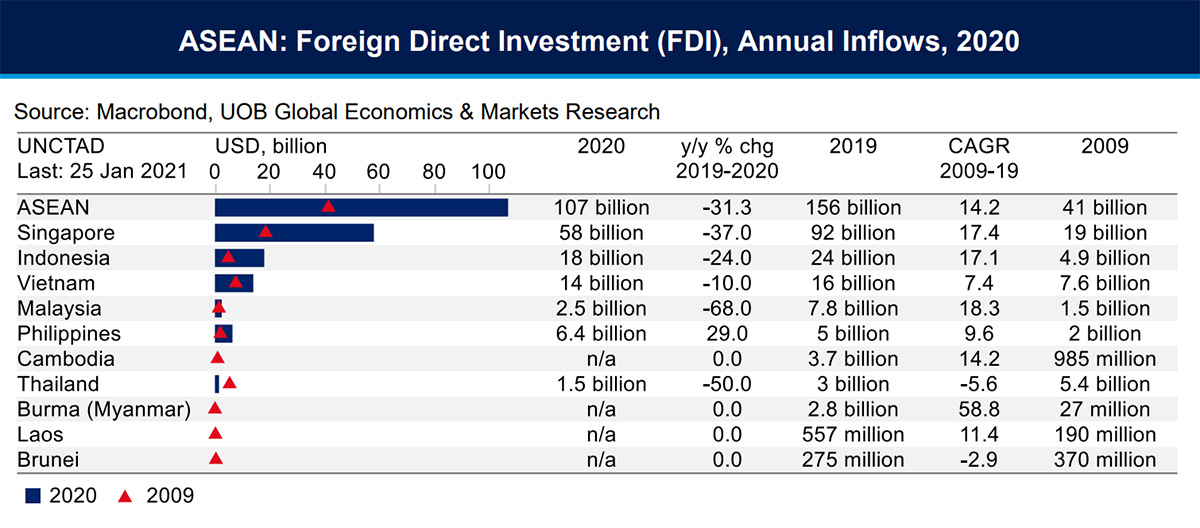

Within the ASEAN region, performance among the members was uneven in 2020. The Philippines, Vietnam and Indonesia performed relatively better than their major peers, while Malaysia and Thailand experienced sharp declines in FDI inflows.

Philippines

Philippines was the lone exception within ASEAN, with a positive 29 per cent growth in FDI inflows in 2020. This comes despite the weight of COVID-19 infections, as the country reported its worst GDP recession on record and the worst performance among major ASEAN economies.

Vietnam

FDI inflows to Vietnam declined at a more moderate pace compared to its ASEAN neighbours as the country was able to control the COVID-19 pandemic for most of 2020. As a result, economic activities expanded 2.9 per cent during the year, one of the few Asian economies that was able to accomplish such a feat, with a sharp growth rebound expected in 2021. In addition, relocation of supply chains and infrastructure investments continued during the year, which helped sustain FDI inflows.

Indonesia

Indonesia performed slightly better than its peers during the year, with inflows falling a relatively mild 24 per cent, to US$18 billion. The outlook for FDI inflows ahead looks promising as the country managed to achieve its overall investment targets in 2020. The recently passed Omnibus Law could potentially elevate Indonesia’s cost competitiveness and efficiency.

Malaysia

Malaysia experienced the worst decline in FDI inflows within ASEAN in 2020, partly hurt by both ongoing political uncertainty and movement restrictions in response to the COVID-19 pandemic throughout the year, delaying some investment decisions. However, with investment approvals in the first nine months of 2020 exceeding MYR100 billion, particularly with strong gains in investment approvals in the manufacturing sector (+16.6 per cent year-on-year), the actualisation of these approvals should pave the way for further inflows in 2021 and beyond.

Skyscrapers in Kuala Lumpur, capital of Malaysia. Although Malaysia recorded the worst decline in FDI inflows within ASEAN in 2020, it has received investment approvals exceeding MYR100 billion as of 3Q2020, which should encourage further FDI inflows. Photo: Pawel Szymankiewicz / Unsplash

Thailand

Thailand was the second worst performer in terms of FDI inflows in 2020 within the ASEAN bloc, which UNCTAD attributed to a divestment of a foreign-owned supermarket chain to a Thai investor group during the year. Historically, Thailand’s FDI performance has lagged its peers by a wide margin (CAGR of -5.6 per cent vs. 14.2 per cent for overall ASEAN). The outlook for Thailand could be challenging as competition for investment is likely to remain fierce in the years ahead.

Singapore

As a regional and financial hub, Singapore has traditionally enjoyed large FDI inflows compared to other ASEAN members. However, the COVID-19 pandemic and a slump in business activities globally saw FDI inflows to Singapore contracting by 37 per cent to US$58 billion, worse than the overall decline of 31 per cent for ASEAN. This is largely due to an 86 per cent plunge in cross-border M&As as foreign acquisitions slowed in the region, according to UNCTAD.

Nevertheless, the outlook for Singapore’s FDI inflows remains positive, as regional economies are expected to see a growth rebound in 2021, which would be favourable to Singapore’s role as an investment funnel to the region.

Within Singapore, there are other positive factors that will attract investment inflows in the years ahead, such as an open economy, external connectivity, and business continuity, among others. Singapore managed to attract S$17.2 billion (US$12.7 billion) in fixed asset investments in 2020 – the largest amount since 2008 and well above the official mid- to long-term target of S$8-10 billion – despite weathering its worst recession since independence. Furthermore, Singapore has targeted to grow its manufacturing sector by 50 per cent over the next 10 years as it works to ensure that the sector continues to contribute about 20 per cent of economic output over the medium term. The signing of RCEP (Regional Comprehensive Economic Partnership) will be another catalyst as companies relocate and reconfigure supply chains in a post-pandemic world.

Figure 2: FDI inflows into ASEAN in 2020

While performance differed among members, overall for ASEAN, the setback from the COVID-19 pandemic and slump in the global economy has resulted in a relatively more moderate impact on investment inflows (-31 per cent), compared to the world (-42 per cent). UNCTAD has warned that FDI is expected to remain weak in 2021 (forecast: -5 per cent to -10 per cent), and with forward indicators pointing to continued downward pressure.

Nevertheless, historically ASEAN and its members have generally outperformed the competition for FDI inflows, with a compound annual growth rate (CAGR) of 14 per cent over the 2009-19 period, far ahead of the 5.2 per cent pace for China and 6.2 per cent for the US. This is largely due to the stability in the region, and an openness to foreign investments. Meanwhile, the addition of RCEP will be another catalyst for ASEAN’s prospects ahead.

RCEP: Key catalyst for further FDI inflows into ASEAN

After eight years of negotiations, the Regional Comprehensive Economic Partnership (RCEP) free trade agreement (FTA) involving all 10 ASEAN member countries, China, Japan, South Korea, Australia and New Zealand, was signed in November 2020. This agreement will be one of the key growth drivers for the 15-member FTA in the coming decades as the regional bloc will be increasingly more economically integrated.

RCEP is the world’s largest FTA, covering 30 per cent of the world’s GDP and world’s population, and 27 per cent of the world’s total trade (i.e. merchandise exports and imports) value in 2019. Furthermore, RCEP members produced nearly half of the world’s manufacturing output.

There are several factors that will be attractive to investors looking to deploy their FDI flows into RCEP:

1. RCEP’s adoption of a harmonised Rules of Origin (ROO) will allow ample opportunities for the shifting and diversification of supply chains within RCEP, especially in light of the COVID-19 pandemic and uncertainty in US-China relationship. Additionally, it is also attractive for non-RCEP/third country companies looking to produce and export to RCEP members, especially to the rising ASEAN market as well as China, which is adopting a “dual circulation” economic strategy and projecting to double the size of its economy by 2035.

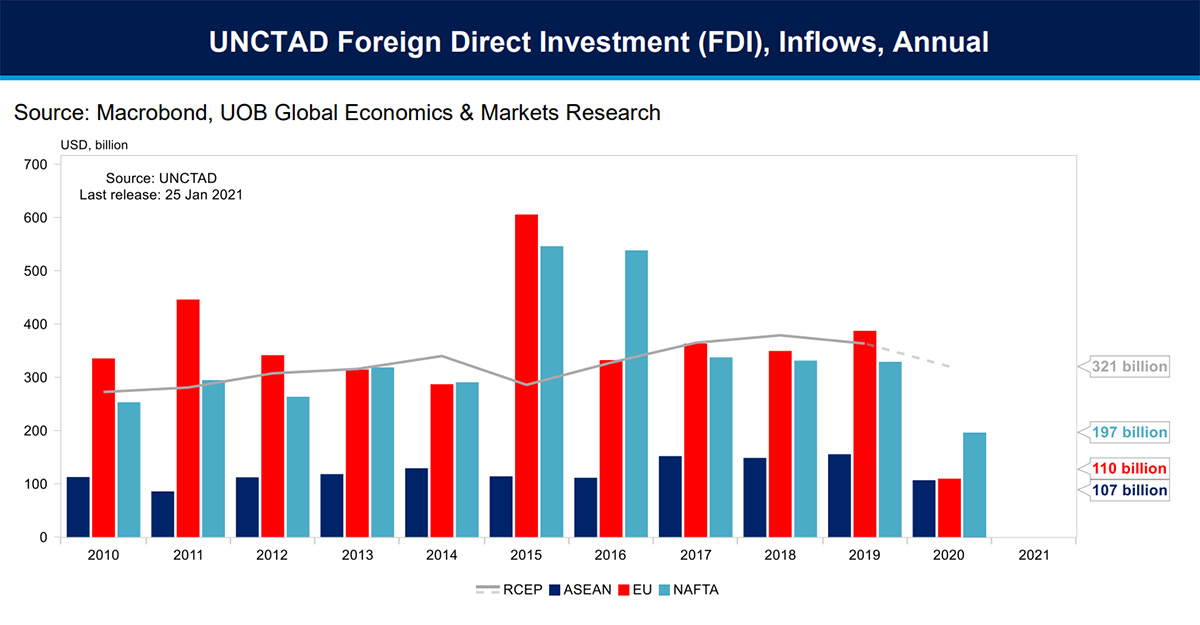

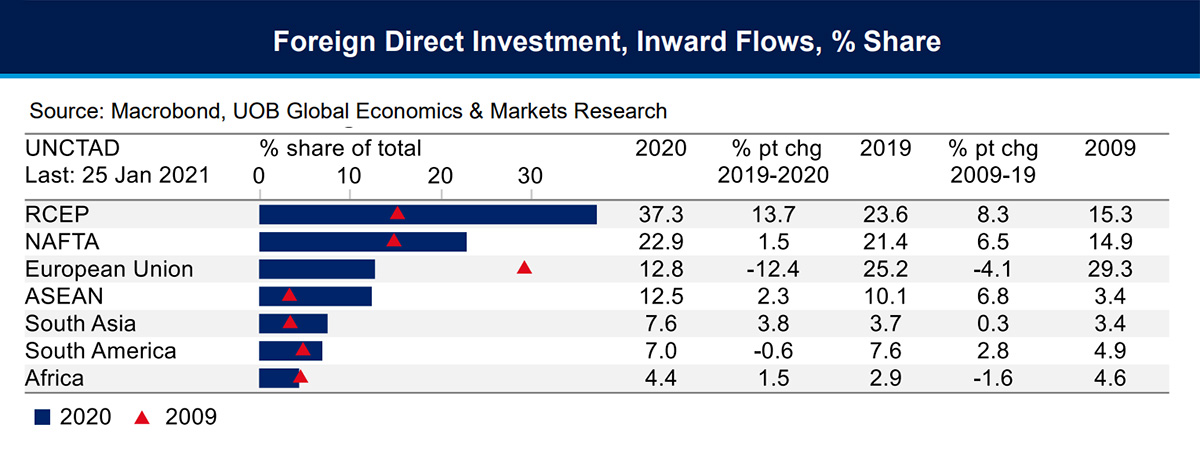

2. In terms of FDI inflows, RCEP as a grouping has been a main investment destination in recent years, due to the size of its economy, as well as a highly diverse range of countries with varied degrees of economic development, cost structures and resource endowments. FDI inflows into RCEP accounted for 37 per cent share of global FDI inflows in 2020, an increase of nearly 12 per cent points from 2019, and well ahead of another more established grouping, NAFTA (now called USMCA or United States-Mexico-Canada Agreement on trade). On the other hand, the share for the European Union (EU) in FDI inflows has fallen steadily through the years, from 29 per cent in 2009 to 13 per cent in 2020.

Figure 3: FDI inflows based on trade blocs, 2010-2020. Source: UNCTAD

Figure 4: FDI inflows based on trade groupings, 2009 vs. 2020

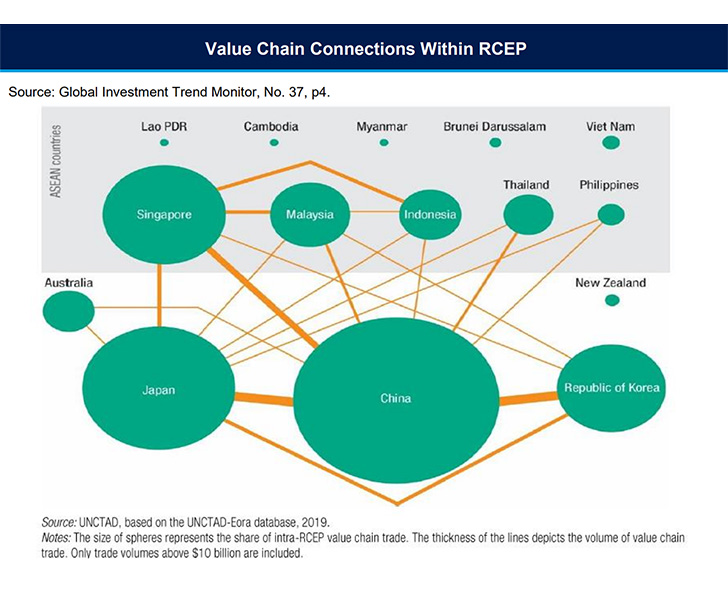

3. RCEP is highly integrated into the global value chains (GVC), accounting for 26 per cent of the world’s GVC trade volume (in both trade in goods and services), according to the United Nations. In addition, intra-regional value chain trade within RCEP has grown even faster, rising 50 per cent over the 2010 level to US$1.7 trillion in 2017. However, GVC in RCEP is centred on large and established hubs such as China, Japan, and South Korea, giving room for trade and investment opportunities for peripheral countries such as Vietnam and Myanmar.

The UN study also noted that GVC patterns are closely connected to FDI patterns, with the top five GVC industries in RCEP absorbing more than 50 per cent of the value of greenfield investment project announcements. In RCEP, the GVC is dominated by five industries, namely electrical and machinery, petroleum and chemicals, metal, textile and apparel, and transport equipment. These industries collectively account for 60 per cent of RCEP’s total GVC trade.

With RCEP the leading destination for global FDI inflows in recent years, this position is likely to be entrenched further once the FTA comes into force (currently awaiting ratification by various governments). In addition, the region’s deep-rooted GVC participation, China’s dual circulation strategy, and ASEAN’s rising population and income will also be the main drivers for further investments into the region and ASEAN.

Important notes and disclaimers

This article shall not be copied, or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

About the author

Suan Teck Kin

UOB

Suan Teck Kin joined UOB as an economist in 2006. In his current role as Executive Director in Global Economics and Markets Research, he is responsible for macroeconomic and foreign exchange research with a primary focus on China, Hong Kong SAR and Taiwan, and secondary coverage for the ASEAN region. As a member of the Research team, he presents the team’s market views regularly to the Bank’s management team and clients in Singapore and the region.

Teck Kin has more than 10 years of experience in macroeconomics and equity research. Fluent in English and Mandarin, Teck Kin is interviewed frequently by local and international print and broadcast media, as well as financial newswires on the economic and market outlook.