Indonesia: 2Q21's FDI increased by 19.6 per cent year-on-year

Trade & Investments

27 Jul 2021

3 mins read

You are now reading:

Indonesia: 2Q21's FDI increased by 19.6 per cent year-on-year

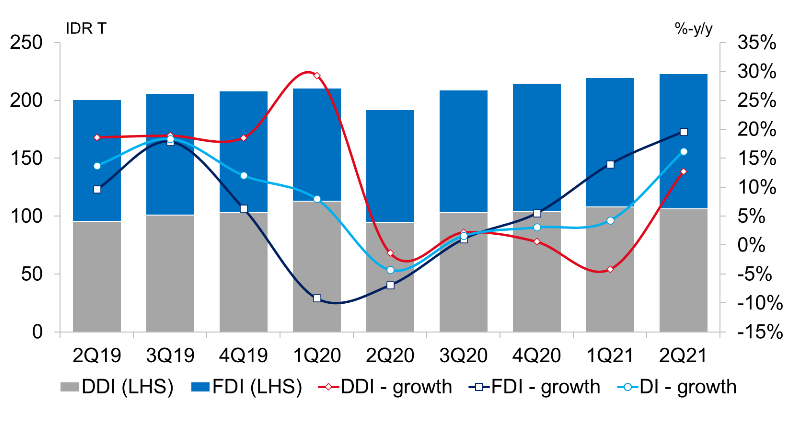

Indonesia’s direct investment rose by 16.2 per cent year-on-year from April to June 2021 vs. 4.3 per cent in the previous quarter, underpinned by the positive performance of both foreign direct investment (FDI) and domestic direct investment (DDI). The continued sustained rise in FDI into Indonesia suggests that despite the pandemic, global and regional interests into the country’s mid- to long-term prospects remain intact. We share the relatively sanguine view that with the country’s rapid vaccination drive underway, the Indonesian economy should be able to open up more sustainably and receive an even greater flow of direct investments ahead.

Below is a snapshot of the second quarter’s performance.

1. FDI and DDI growth

The data from the Investment Coordinating Board Indonesia (Badan Koordinasi Penanaman Modal – BKPM) showed FDI grew by 19.6 per cent year-on-year to IDR 116.8tr in 2Q21 (equivalent to US$8.0bn, using this year’s national budget IDR exchange rate assumption of IDR 14,600 per US$) vs. 1Q21’s 14.0 per cent.

BKPM reiterated that the enactment of Law Number 11 of 2020 concerning Job Creation and its technical guidelines have created positive sentiments for investors to keep their investments activities. Moreover, DDI increased by 12.7 per cent to IDR 106.2tr (US$7.3bn) in 2Q21 vs. 4.2 per cent contraction in 1Q21, partly due to low base effect in 2Q20 (see Figure 1 below).

Figure 1: Investment realisation growth 2Q21. Source: Investment Coordinating Board Indonesia, UOB Global Economics and Markets Research

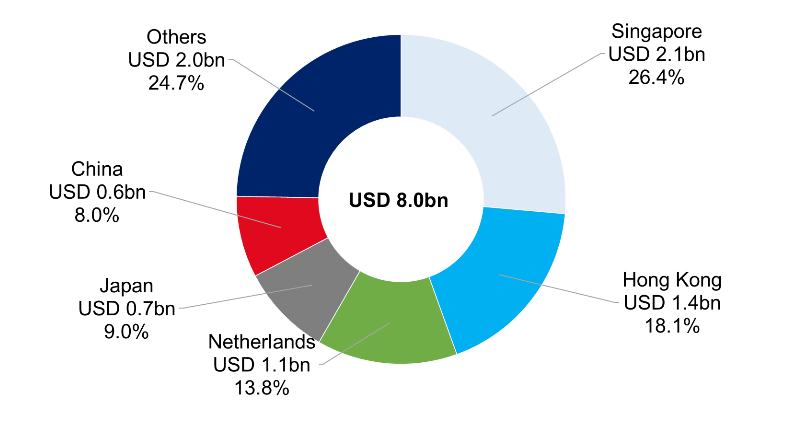

2. Top sources of foreign investment

Singapore remained as the largest foreign investor in Indonesia, with investment valued at US$2.1bn for 3,821 projects, followed by Hong Kong at US$1.4bn for 615 projects (see Figure 2). Meanwhile, Netherlands climbed up the ranks to third place with investment valued at US$1.1bn for 614 projects.

Figure 2: Top five FDI 2Q21 by country of origin. Source: Investment Coordinating Board Indonesia, UOB Global Economics and Markets Research

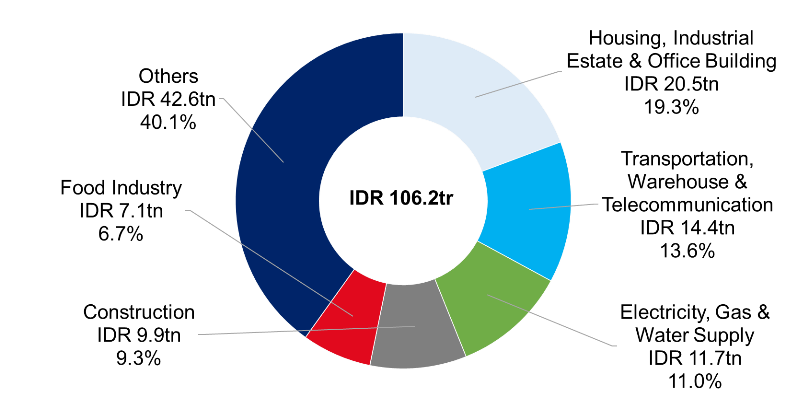

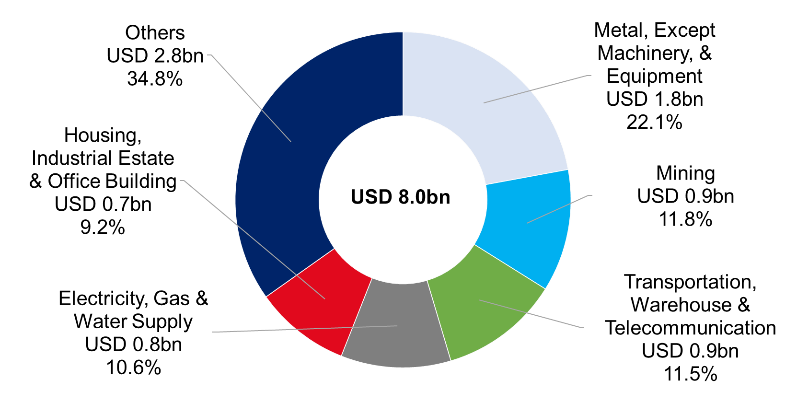

3. Key sectors receiving direct investments

The housing, industrial estate and office building sector was the largest recipient of DDI in 2Q21, valued at IDR 20.5tr (US$1.4bn, see Figure 3).

Meanwhile, metal (except machinery and equipment) was the leading sector for FDI at US$1.8bn (see Figure 4).

Figure 3: Top five DDI 2Q21 by sector. Source: Investment Coordinating Board Indonesia, UOB Global Economics and Markets Research

Figure 4: Top five FDI 2Q21 by sector. Source: Investment Coordinating Board Indonesia, UOB Global Economics and Markets Research

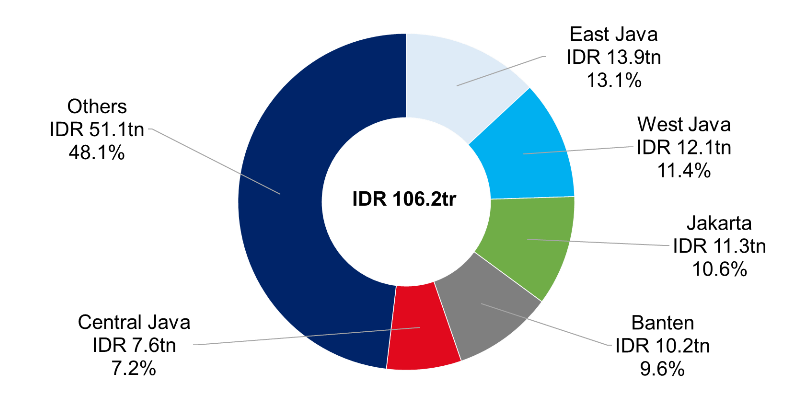

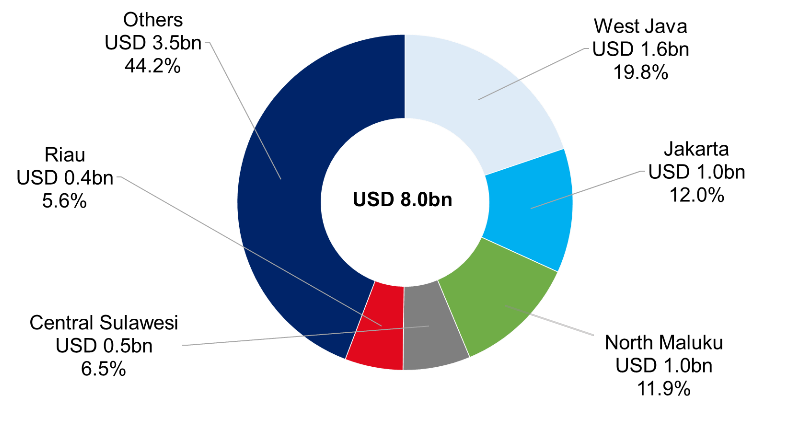

4. Top five destinations for investments

The top five destinations for investments in 2Q21 were West Java, Jakarta, East Java, Banten, and North Maluku (see Figures 5 and 6 below).

Figure 5: Top five DDI 2Q21 by location. Source: Investment Coordinating Board Indonesia, UOB Global Economics and Markets Research

Figure 6: Top five FDI 2Q21 by location. Source: Investment Coordinating Board Indonesia, UOB Global Economics and Markets Research

KPM said that business has become accustomed to the coronavirus pandemic, which helped spur investment flows into Southeast Asia’s largest economy. However, the rising COVID-19 cases and stricter coronavirus curbs beginning in July will likely affect the 3Q21 FDI numbers. From January to June, the achievement of investment realisation has contributed 49.2 per cent to the target of 2021 of IDR 900tr, and it has successfully absorbed 311,922 Indonesian workers.

Moving forward, BKPM is still optimistic that the investment realisation target will likely be achieved under the expectation that the COVID-19 pandemic situation can be controlled.

Important notes and disclaimers

This article shall not be copied, or relied upon by any person for whatever purpose. This article is given on a general basis without obligation and is strictly for information only. The information contained in this article is based on certain assumptions, information and conditions available as at the date of the article and may be subject to change at any time without notice. You should consult your own professional advisers about the issues discussed in this article. Nothing in this article constitutes accounting, legal, regulatory, tax or other advice. This article is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Although reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this article, UOB and its employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accept no responsibility or liability for any error, inaccuracy, omission or any consequence or any loss or damage howsoever suffered by any person arising from any reliance on the views expressed and the information in this article.

About the authors

Enrico Tanuwidjaja

UOB Indonesia

Enrico Tanuwidjaja is the Economist at UOB Indonesia. He joined UOB Indonesia in 2017 and is responsible for macroeconomic research focusing on Indonesia. Enrico writes on the Indonesian macroeconomic development and outlook as well as on the domestic financial market, giving insights for UOB's internal and external clients. Enrico is regularly featured in reputable news and business media, including writing opinion pieces. Follow him on LinkedIn

Haris Handy

UOB Indonesia

Haris Handy is a research associate at UOB Indonesia. He joined UOB Indonesia in 2017 and is responsible for macroeconomic research focusing on Indonesia, providing insights and information for UOB’s internal and external clients. Follow him on LinkedIn

Find out how we can help your business expand across ASEAN. Get in touch