Balancing Growth with Stability for the Long Term / Financial Highlights

Financial Highlights

Resilient earnings driven by strong fee momentum across our diversified franchise

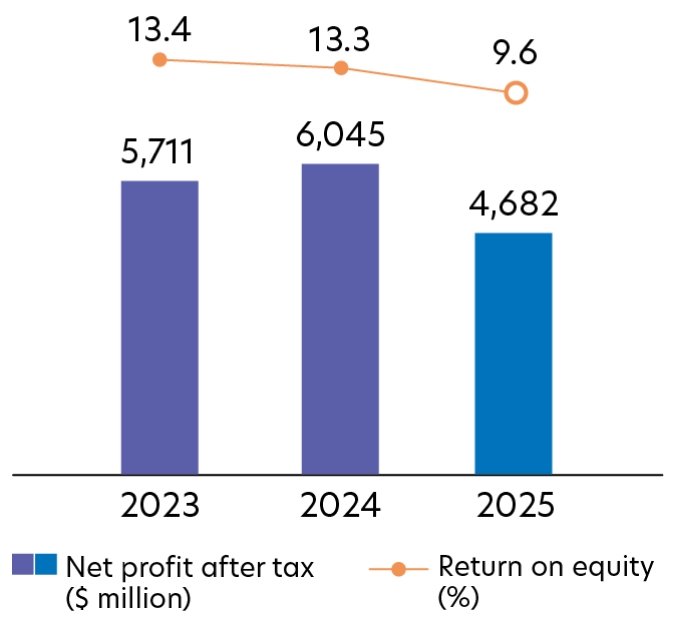

Net Profit After Tax and Return on Equity

Net profit moderated 23% to $4.7 billion primarily due to the Group's proactive decision to strengthen coverage through pre-emptive provisioning in light of evolving macroeconomic conditions and sector-specific challenges.

Net Profit After Tax

$4.7

billion

- 23%

Return on Equity

9.6

%

- 3.7% pt

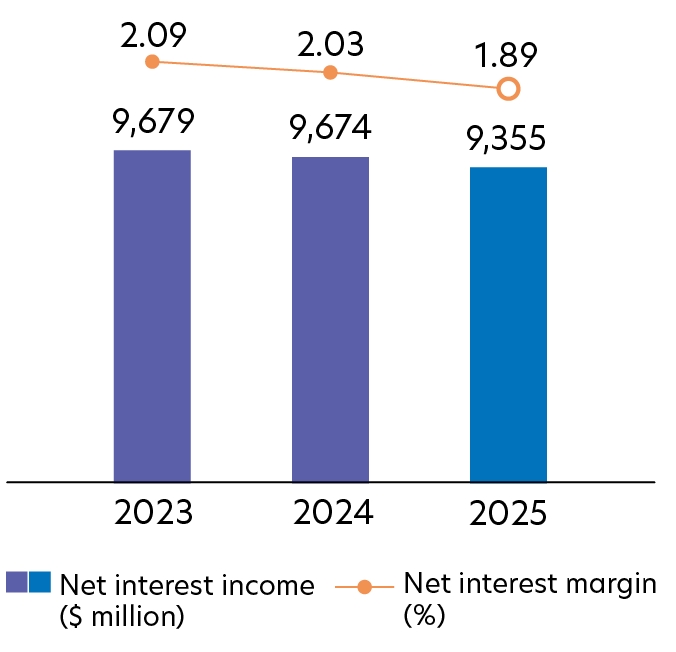

Net Interest Income and Margin

Net interest income fell 3% year on year to $9.4 billion as net interest margin narrowed 14 basis points to 1.89% on the back of lower benchmark rates, cushioned by asset growth.

Net Interest Income

$9.4

billion

- 3%

Net Interest Margin

1.89

%

- 0.14% pt

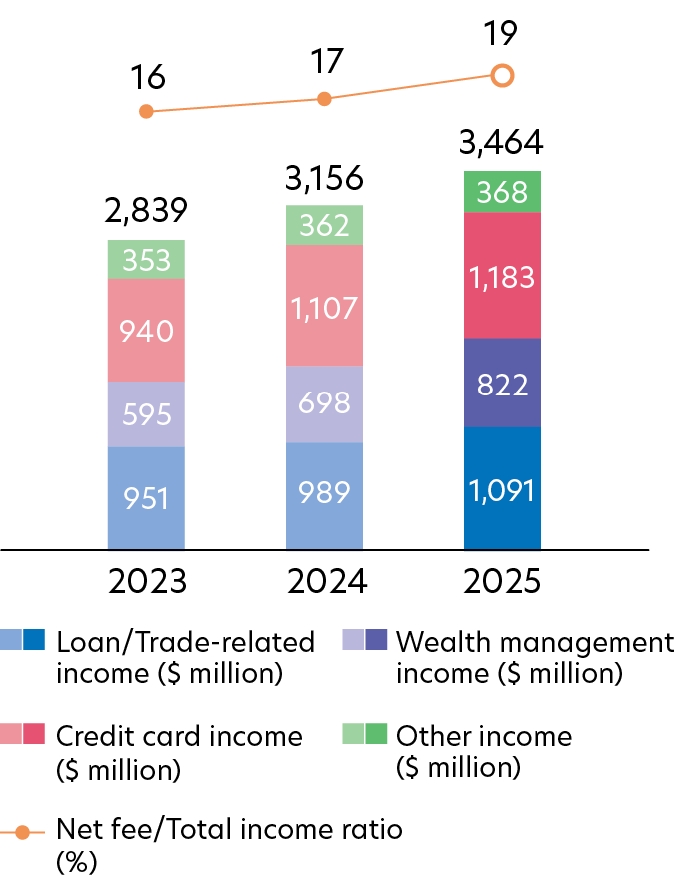

Fee and Commission Income

Gross fee income rose 10% year on year to a new record of $3.5 billion, as wealth management and loan-related fees reached new heights amid favourable market conditions and rising consumer confidence, alongside stronger card fees. On a net basis, fee income grew 7% year on year to $2.6 billion.

Note: Fees presented are gross of expenses, unless stated otherwise

Net Fee Income

$2.6

billion

+ 7%

Net Fee/Total Income

Ratio

Ratio

19

%

+ 2% pt

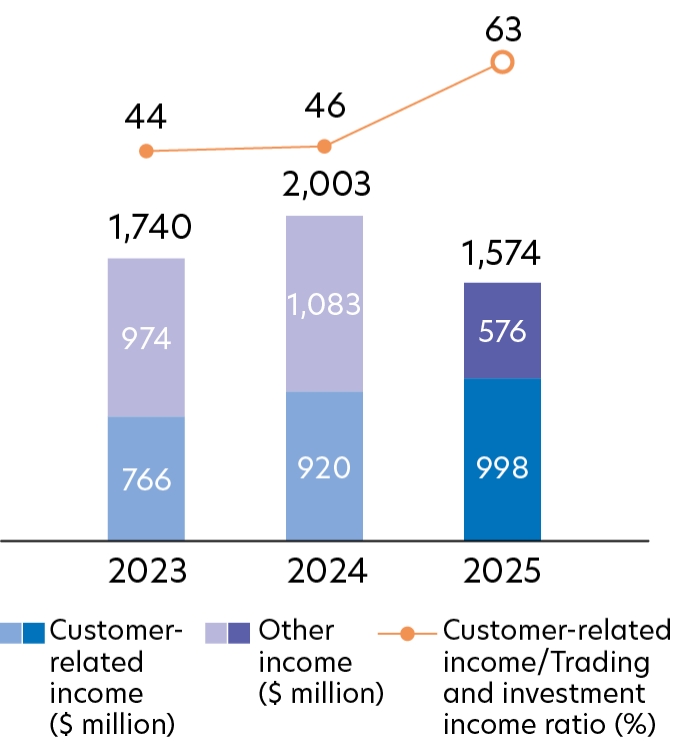

Trading and Investment Income

Trading and investment income came in at $1.6 billion, down 21% from a year ago as trading income and liquidity management activities normalised following last year’s exceptional performance. Customer-related treasury income however registered an all-time high fuelled by strong hedging and investment demand.

Trading and Investment Income

$1.6

billion

- 21%

Customer-related Income

$1.0

billion

+ 8%

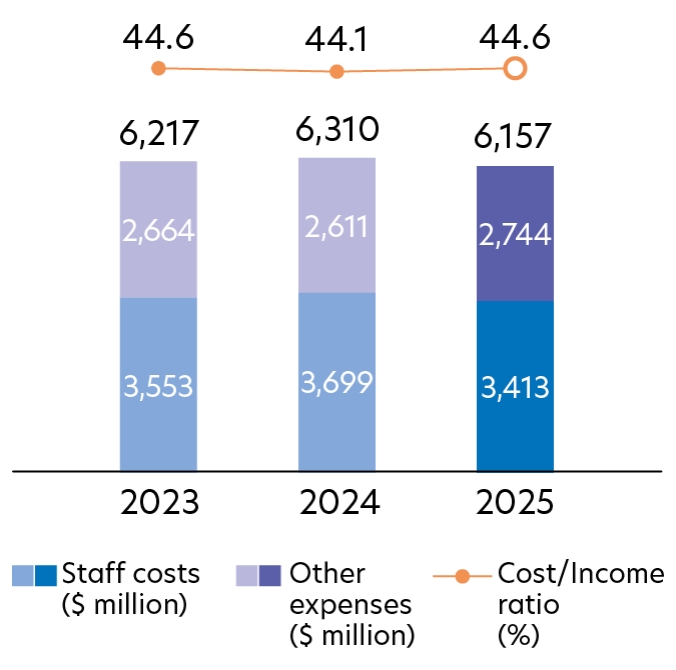

Operating Expenses

Total operating expenses edged down 2% year on year, with cost-to-income ratio at 44.6%, supported by active cost discipline alongside targeted strategic investments.

Operating Expenses

$6.2

billion

- 2%

Cost/Income Ratio

44.6

%

+ 0.5% pt

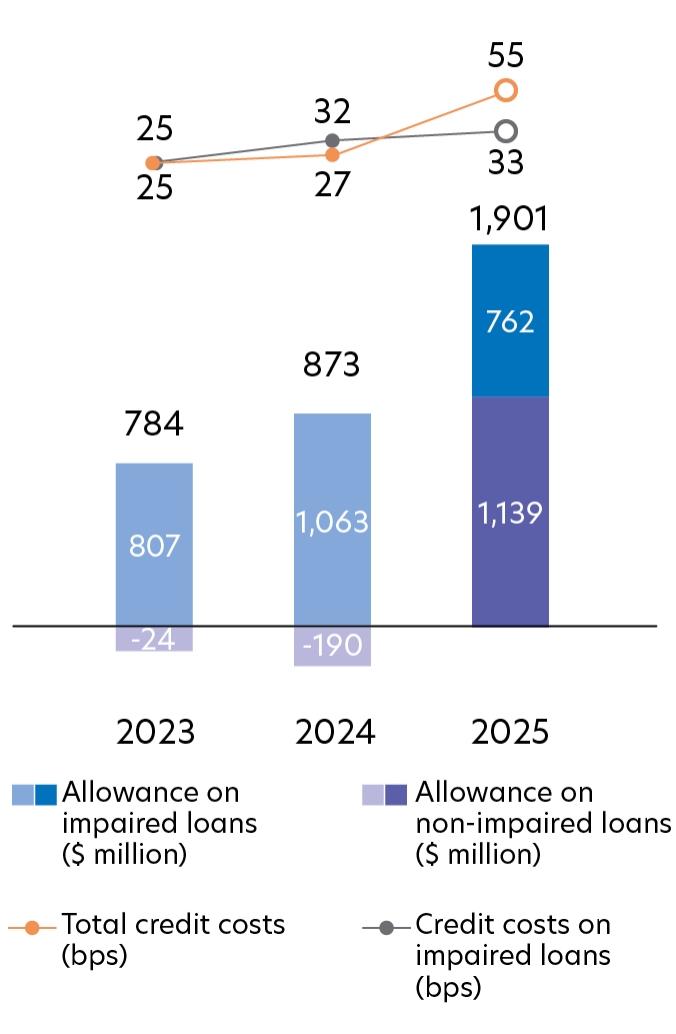

Total Allowance on Loans

Total allowance on loans rose to $1.9 billion in 2025, reflecting pre-emptive provisioning to further reinforce the Group's balance sheet strength.

Total credit costs on loans were 55 basis points.

Total credit costs on loans were 55 basis points.

Total Allowance

on Loans

on Loans

$1.9

billion

> 100%

Total Credit Costs

55

bps

+ 28 bps

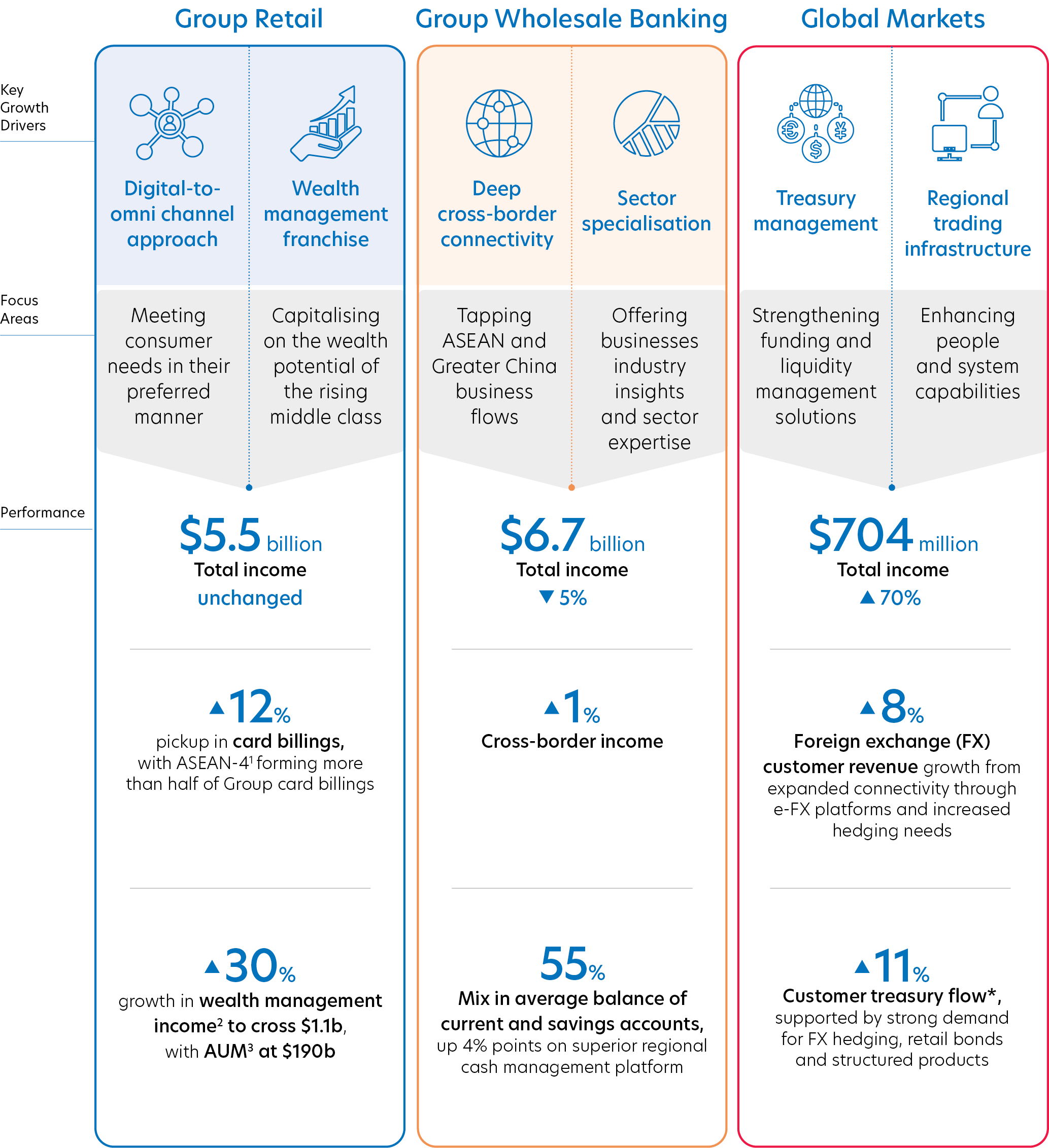

Staying focused on our regional strategy and customer centricity

Group Retail

Group Wholesale Banking

Global Markets

Deepening customer relationships across ASEAN

Wealth management franchise

Key

Growth

Drivers

Growth

Drivers

Leveraging our regional strength and depth of offerings to meet rising consumer needs across life stages

Capitalising on the wealth potential of the rising middle class

Focus

Areas

Areas

$5.1

billion

Total income

7%

Performance

8

%

Pickup in card billings,with ASEAN-41 forming more thanhalf of Group card billings

$201

billion

AUM2, with wealth management income3 up 14% to $1.3b

Deep

cross-border connectivity

cross-border connectivity

Sector specialisation

Tapping ASEAN and Greater China business flows

Offering businesses industry insights and sector expertise

$6.2

billion

Total income

7%

27

%

Mix in cross-border income, with 1% point increase

61

%

Mix in balance of current

and savings accounts,

up 4% points on superior regional cash management platform

and savings accounts,

up 4% points on superior regional cash management platform

Treasury management

Regional trading infrastructure

Strengthening funding and liquidity management solutions

Enhancing people and system capabilities

$1.1

billion

Total income

51%

3

%

Foreign exchange (FX) customer revenue growth from expanded connectivity through e-FX platforms and increased hedging needs

4

%

Customer treasury flow*, supported by strong demand for hedging and wealth solutions

*

Income derived from the treasury flow from Group Retail and Group Wholesale Banking customers is reflected in the income of the respective business segments.

1

ASEAN-4 comprises Indonesia, Malaysia, Thailand & Vietnam

2

Refers to Privilege Banking and Private Bank

3

Comprises wealth management fees and customer-related treasury income

Operating Income by Business Segment

Group Retail

Total income eased 7% to $5.1 billion, reflecting the backdrop of falling interest rates and intense competition across key markets. Despite these headwinds, the underlying franchise delivered growth, achieving a double-digit trajectory in wealth management income and CASA balances, supported by strong customer value propositions.

Group Wholesale Banking

Total income reduced 7% amid lower interest rates and keen competition for quality clients across the banking industry. This was partially cushioned by record-high investment banking fees, double-digit growth in CASA and trade assets backed by pan-regional transaction banking platforms, and healthy treasury customer flows.

Global Markets

Total income soared 51% to $1.1 billion, led by lower funding costs, alongside growth in activities across foreign exchange and equities.

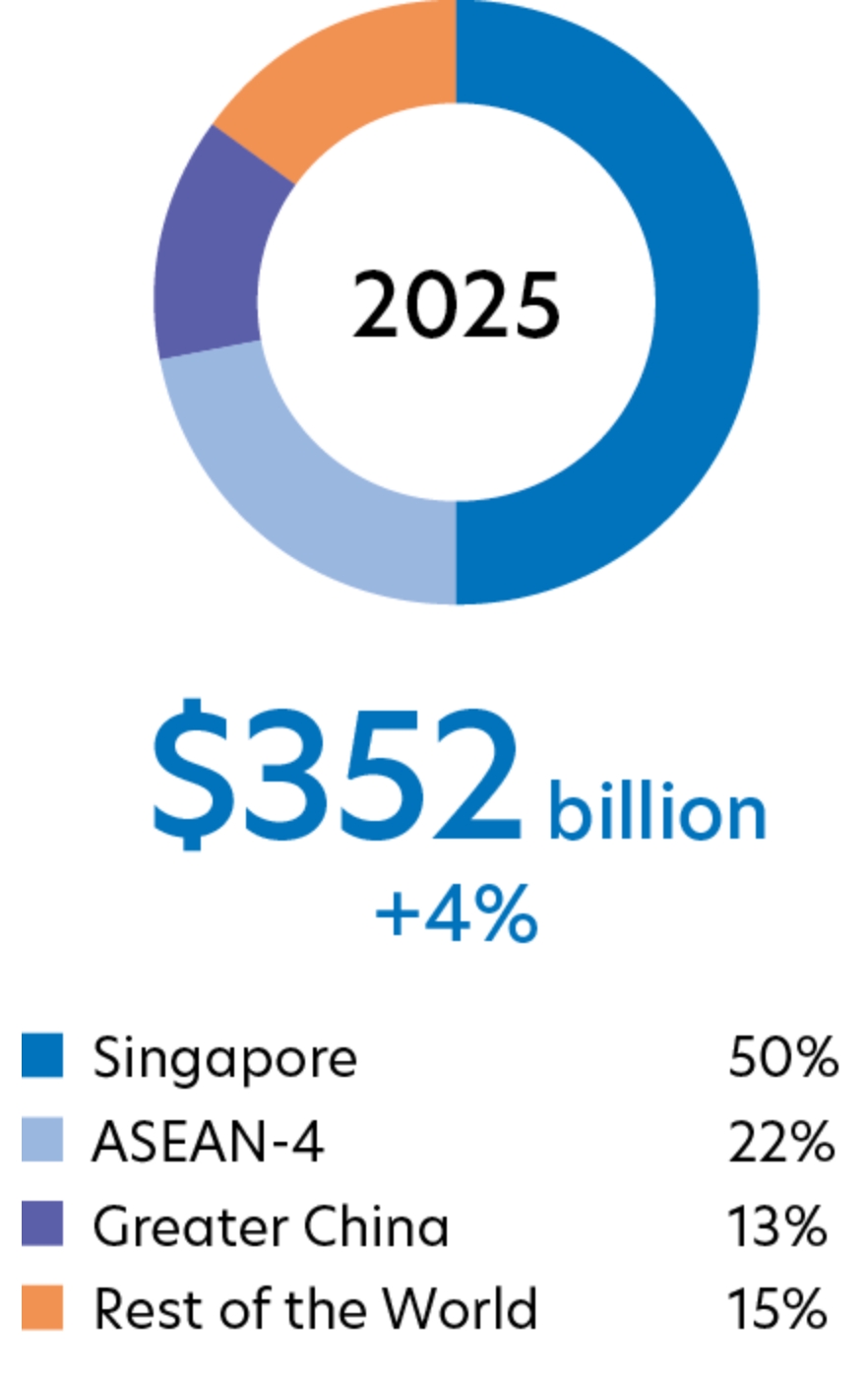

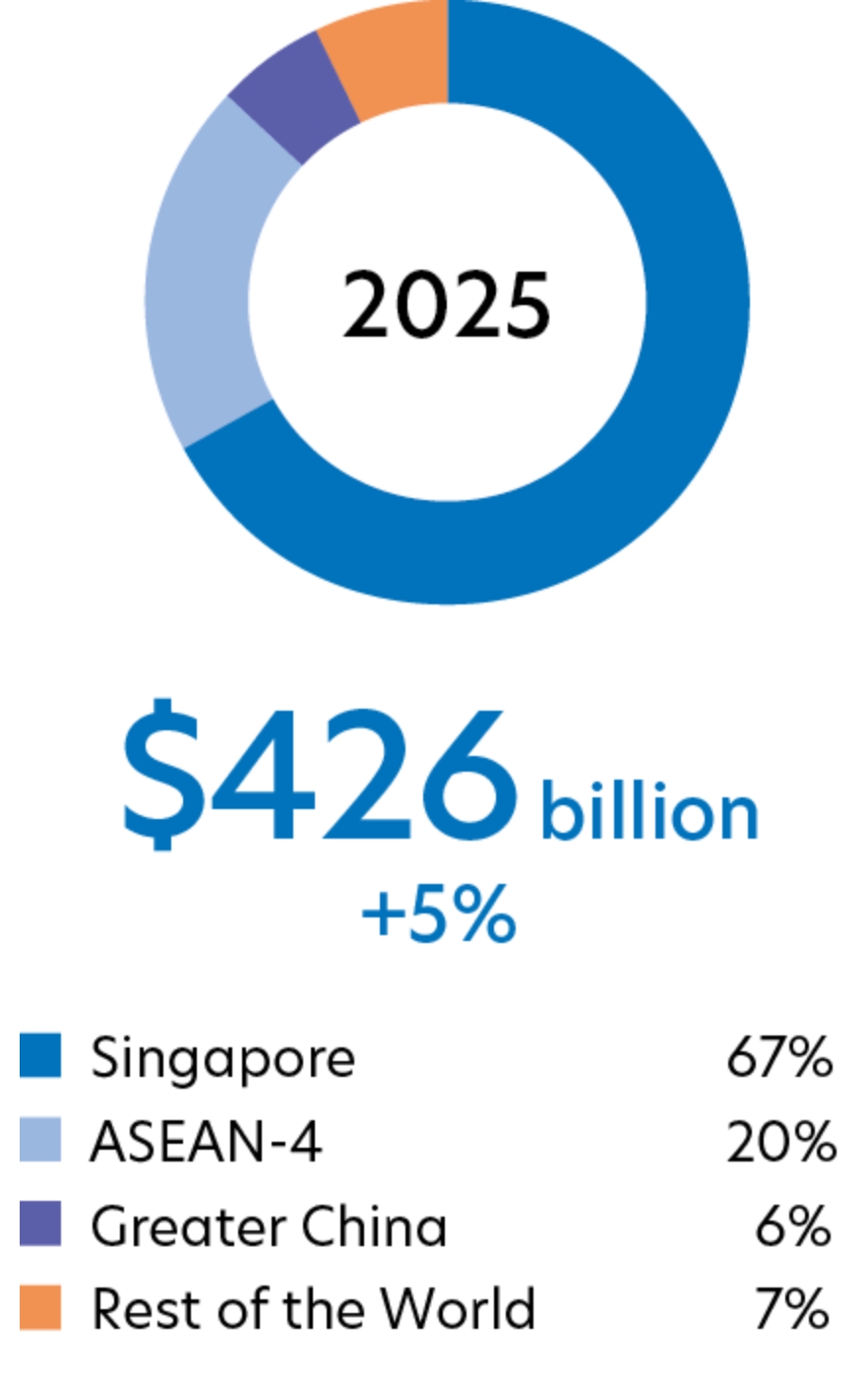

Operating Income by Geographical Segment

Overseas franchise provided diversification and cross-border connectivity

$ million

2025

2024

YoY (%)

Singapore

7,549

8,059

(6)

ASEAN-4

3,940

3,770

5

Malaysia

1,656

1,511

10

Thailand

1,470

1,478

(1)

Indonesia

639

629

2

Vietnam

175

152

15

Greater China

1,155

1,230

(6)

Rest of the World

1,164

1,235

(6)

Total

13,808

14,294

(3)

Customer Loans1

Customer Deposits

Singapore

Total income declined 6% from a year ago. Net interest income eased 6% year on year to $5.1 billion due to lower benchmark rates and competitive pricing, partially cushioned by active balance sheet management and quality asset growth. Non‑interest income fell 8% to $2.5 billion as lower trading and investment gains masked record loan fees and double‑digit expansion in wealth management income.

Greater China

Total income moderated 6% year on year to $1.2 billion due to softer performance in proprietary trading, investment, loan and wealth, partially cushioned by higher net interest income.

ASEAN-4

Total income rose 5% from last year, driven by broad-based client activities across lending, proprietary trading, treasury and wealth management. Faster income growth was recorded in Malaysia and Vietnam due to lower funding costs and asset growth respectively, while a falling rates backdrop moderated the income momentum in Thailand.

Rest of the World

Total income for 2025 fell 6% against a year ago to $1.2 billion mainly due to lower benchmark rates, alleviated by stronger trading and investment gains.

1

Loans by geography are classified according to where credit risks reside, largely represented by the borrower's country of incorporation/operation for non-individuals and residence for individuals.

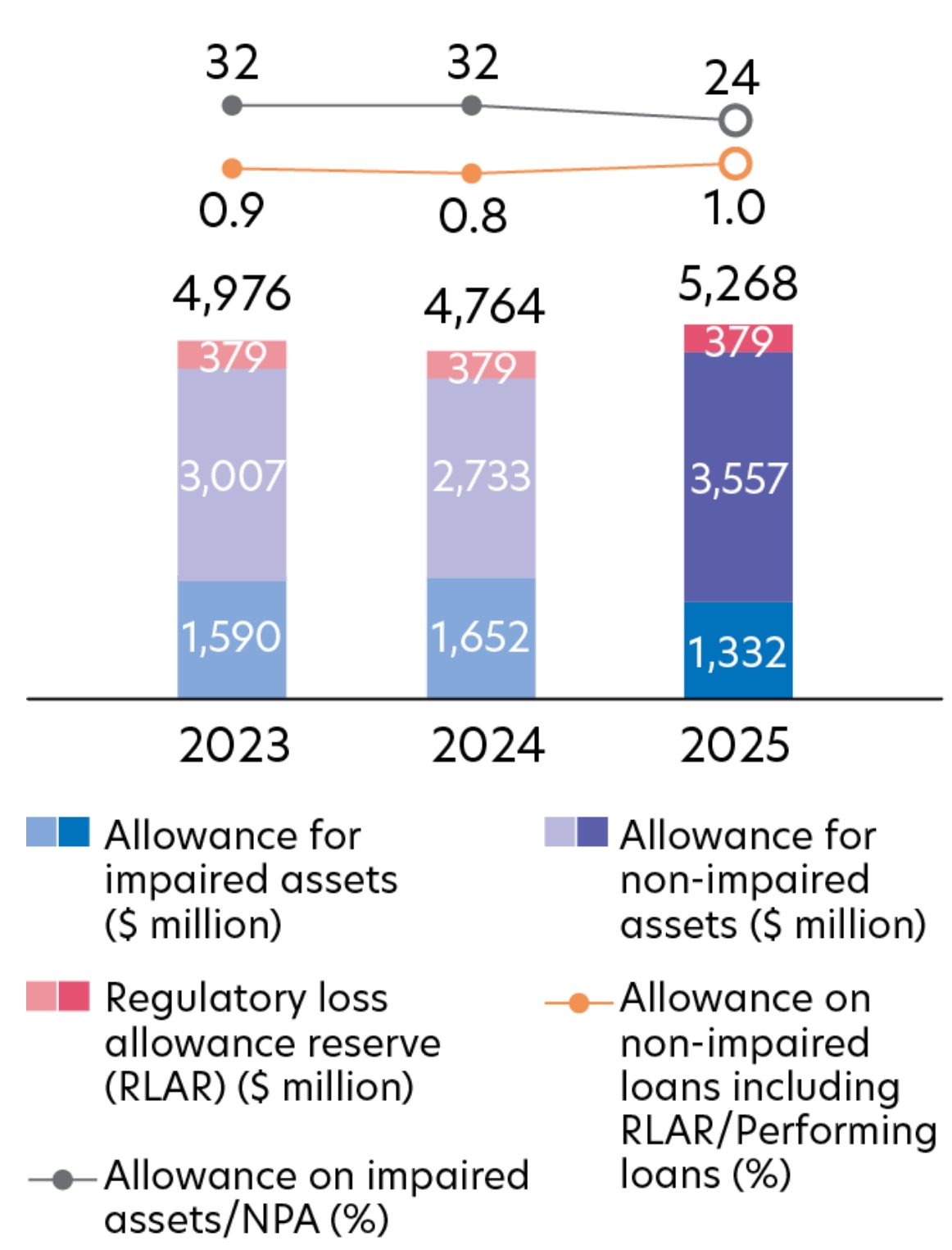

Sound balance sheet with adequate asset coverage

Asset Quality and Allowance Coverage

The Group's performing loans coverage was 1.0% as of 31 December 2025. Non-performing loan (NPL) ratio stood at 1.5%, with non-performing assets (NPA) coverage adequate at 97% or 254% after taking collateral into account.

NPL Ratio

1.5

%

unchanged

Unsecured NPA Coverage

254

%

+ 60% pt

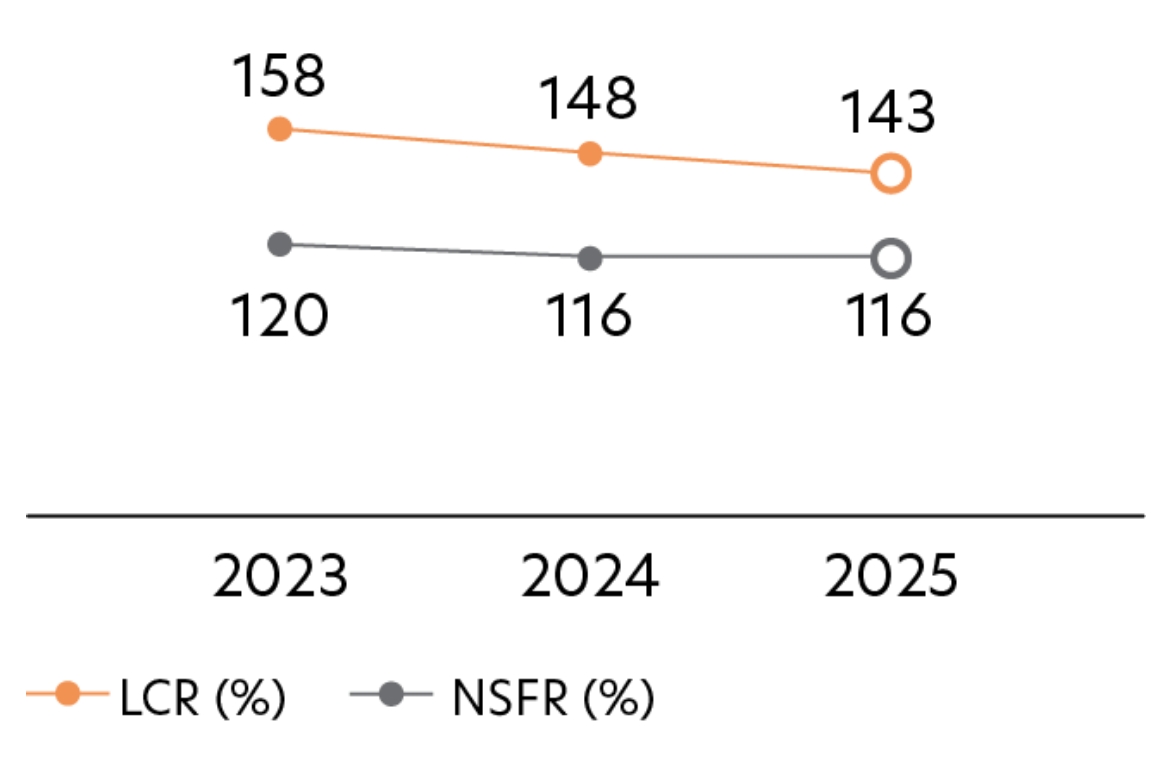

Funding and Liquidity Ratios

The Group’s liquidity remained healthy with the average all-currency liquidity coverage ratio (LCR) at 143% and net stable funding ratio (NSFR) at 116%, well above the regulatory requirements.

LCR

143

%

- 5% pt

NSFR

116

%

unchanged

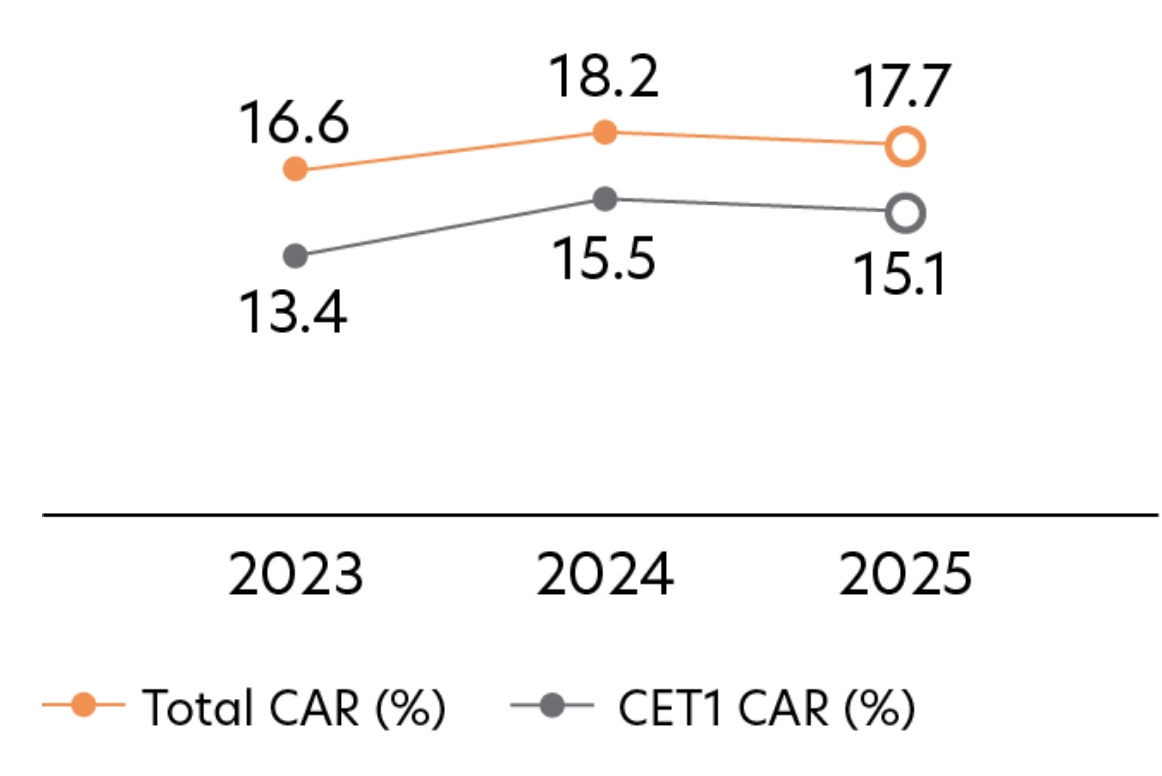

Capital Adequacy Ratio (CAR)

The Group maintained a strong capital position with Common Equity Tier 1 (CET1) CAR and Total CAR at 15.1% and 17.7% respectively.

CET1 CAR

15.1

%

- 0.4% pt

Total CAR

17.7

%

- 0.5% pt

Balancing Growth with Stability for the Long Term

Chairman's Statement

Deputy Chairman and CEO’s Report

Financial Highlights

Investor Highlights

Sustainability Highlights